How to Make Industrial Policy Work Now

Ethan McGowan is a Professor of AI/Finance and Legal Analytics at the Gordon School of Business, SIAI. Originally from the United Kingdom, he works at the frontier of AI applications in financial regulation and institutional strategy, advising on governance and legal frameworks for next-generation investment vehicles. McGowan plays a key role in SIAI’s expansion into global finance hubs, including oversight of the institute’s initiatives in the Middle East and its emerging hedge fund operations.

Input

Modified

Success means steady investment and capacity Milestones and blended finance sustain momentum Run a live portfolio and fix bottlenecks

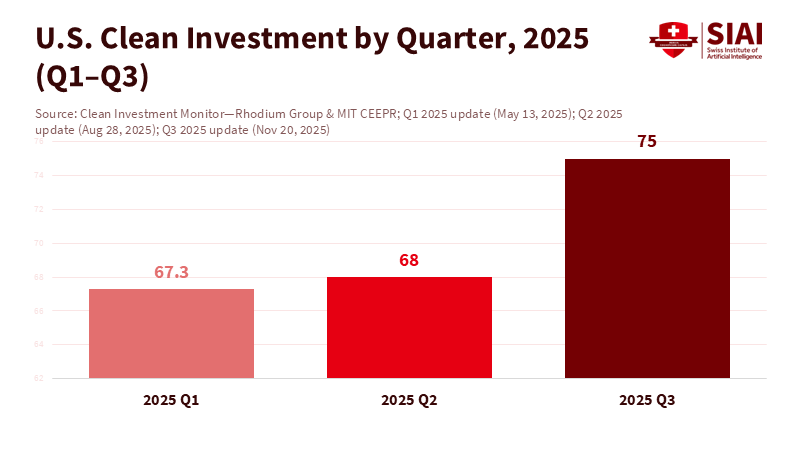

Every policymaker should keep seventy-five billion in mind. In the third quarter of 2025, clean energy and transport projects in the United States attracted $75 billion in new investment, the highest quarterly total ever recorded. This surge did not happen by chance. It resulted from targeted laws, dedicated teams, and a consistent market signal. The key to successful industrial policy lies in sustained, measurable investment that creates factories, increases capacity, and reduces risk in crucial supply chains. The real test is whether programs continue to attract money when the headlines fade. By January 2025, the U.S. Commerce Department had already awarded over $33 billion in CHIPS incentives across 22 states, triggering hundreds of billions in private commitments. Jobs follow money, and milestones help protect it. This is how public funds provide real options for the future rather than just sunk costs. The goal is easy to state but hard to achieve: industrial policy success that builds over time.

Defining Industrial Policy Success

Industrial policy success is not about press releases. It is the steady transformation of public risk-taking into private investment and lasting production capacity at speed. The signs appear in concrete, steel, and production output. One clear indicator is construction spending. U.S. manufacturing construction reached a seasonally adjusted annual rate of about $222 billion in mid-2025, significantly above pre-2022 levels despite tighter financial conditions. This figure matters because it reflects actual work in progress, not just planned projects. Another sign is the consistent flow of clean investments each quarter. In the first two quarters of 2025, clean energy and transport investments remained in the $67–68 billion range before reaching $75 billion in the third quarter. Consistency is more valuable than spikes. This distinction sets successful industrial policy apart from one-time stimulus efforts.

A third sign is the strength of the supply chain that develops around major projects. Battery manufacturing capacity in the U.S. has more than doubled since 2022, reaching over 200 GWh by 2024, with nearly 700 GWh under construction. These figures indicate more than just new facilities; they show that upstream materials, tools, power, and training programs had to be aligned on time. When a state works with a federal agency to design permits, when utilities coordinate grid upgrades with factory requirements, and when awards are distributed based on milestones, the entire system learns by doing. This learning process is the hidden driver of industrial policy success. It helps maintain investment even when economic conditions are unstable. It also explains why "neutral" policies that ignore bottlenecks often fall short.

OECD Guidance and the Limits Toward Industrial Policy Success

The OECD's 12-step checklist serves as a helpful starting point. It emphasizes the importance of using data to diagnose issues, setting measurable goals, defining clear roles across ministries and levels of government, maintaining stable multi-year budgets, and conducting independent evaluations that inform adjustments. It also stresses the need for coordination across government and skilled teams, and for an online tracker to hold programs accountable. These steps are wise. They address the governance backbone that many strategies overlook. Industrial policy success relies on this backbone since complex portfolios cross mandates and election cycles. Without ongoing coordination and regular conflict-resolution routines, even the best-funded program can lose its way.

However, the checklist lacks detail on the complex middle ground where actual deals are made. It advises "embed evaluation," yet does not firmly push for milestone-based funding, clawbacks, equity or warrants, or competitive award design. It calls for "secure, stable budgets." Still, it does not confront shutdown risks or how to protect critical functions when fiscal politics shift. It suggests "collect data," but overlooks the practical question: who controls beneficiary-level data across agencies, and how can it be integrated without delaying delivery? Finally, it downplays what might be called "market choreography." Industrial policy success requires agencies that can identify chokepoints (e.g., EUV light sources, advanced packaging, grid transformers), organize competitive calls around them, and renegotiate as technology and costs change. Guidance should evolve from principles into playbooks that detail the tools and timelines.

United States versus Asia: What Industrial Policy Success Looks Like

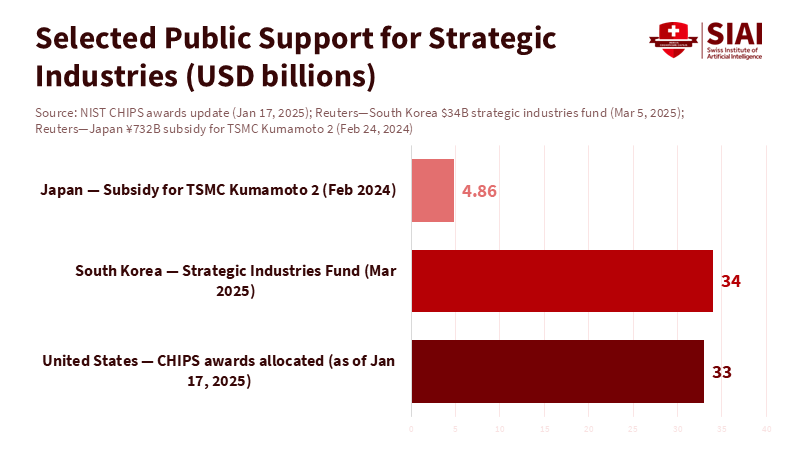

The U.S. experience since 2022 illustrates what effective execution can achieve—and where there are still gaps. By January 2025, the CHIPS Program Office had made 19 awards totaling $30.7 billion in grants and $5.5 billion in loans for semiconductors. The program releases funds when recipients meet milestones. This approach is significant. It lowers the risk of execution for taxpayers and holds firms accountable for realistic schedules. The Commerce Department also reported that over $33 billion in proposed incentives had been allocated by mid-January 2025, with private investment announcements nearing $450 billion since 2021. These figures are not an endpoint; they set the benchmark for what "crowding in" looks like. They also show why industrial policy success depends on program capacity as much as on legal authority.

Manufacturing construction supports this narrative. Even with a broad slowdown in 2025, the level of manufacturing construction remained historically high. The shift in focus also points to targeted sectors. Electronics-heavy projects—fabs, advanced packaging lines, and power electronics facilities—now account for a much larger share than they did a decade ago. Clean manufacturing adds another facet. The Clean Investment Monitor shows clean investment flows rising to a record in the third quarter of 2025. Together, these data reveal that the policy mix continues to attract capital. Industrial policy success, therefore, means having a high and stable baseline of real-economy building.

In contrast, Asia's recent actions have shown a different approach. Japan has complemented substantial subsidies with an institutional focus. In February 2024, Tokyo committed up to ¥732 billion (about $4.9 billion) to support TSMC's second fab in Kumamoto. Japan also pledged over $6.1 billion to Rapidus to develop domestic 2-nanometer capability. These are significant investments aimed at rebuilding a complete chip supply chain, from logic to packaging. South Korea has layered funding on top of its corporate strength, setting up a $34 billion fund in March 2025 to support strategic industries, particularly semiconductors. The Asian model emphasizes scale and speed through close cooperation between government and industry. The U.S. model focuses on competitive allocation, milestone-based funding, and, more recently, equity options for leading suppliers, as seen in an award that included a federal stake in a startup developing a next-generation EUV light source. Both models can succeed. However, both can fail without effective execution.

Clean-tech supply chains reflect a similar pattern. U.S. battery manufacturing capacity surpassed 200 GWh by 2024, with an additional 700 GWh under construction. As projects begin operations between 2025 and 2027, the focus will shift from building factories to ensuring that grids, ports, and workforce pipelines can keep pace. Japan and Korea start with different challenges: they are export champions with strong supply networks, but they also face aging workforces and energy constraints. For all three regions, the measure of industrial policy success by 2028 will be the amount of firm, domestic capacity along the entire chain and how quickly it can scale without running into shortages. This issue cannot be resolved with just one tax credit or grant. It requires a flexible operating model that anticipates bottlenecks and adjusts tools in real time.

A Playbook to Lock In Industrial Policy Success

What, then, turns good guidance into a functional system? First, consider industrial strategy as a live portfolio. This means creating competitive calls to attract private investment, using clear terms, and offering awards that blend grants or tax credits with loans, guarantees, and targeted equity or revenue sharing. It also means implementing strict contractual milestones, automatic clawbacks, and public dashboards that display program-level progress and unit costs. The CHIPS office's approach of using preliminary terms and tiered funding is a practical example. The Milken Institute's review of U.S. practices offers a second lesson: build capacity for delivery quickly. Government agencies hired commercial talent, established deal teams, and coordinated with state partners. This institutional strength—not just financial resources—explains why investment remained strong through 2025. Continue to prioritize this.

Second, plan for friction and learn transparently. Set short and strict deadlines for permitting in strategic zones—pre-permit locations with grid and water plans in place. Use standardized terms for community benefits so local agreements remain consistent—track construction and commissioning timelines, not just the total awards. Publish annual "market maps" outlining chokepoints—EUV sources, transformers, grid-forming inverters—and hold focused competitions to address them. Maintain a disciplined focus on outcomes: capacity added, costs reduced, and resilience achieved. The quarterly readings from the Clean Investment Monitor serve as a model for public accountability. Industrial policy success is iterative. It is a skill. It improves as governments share what works and discontinue what does not.

The headline figure—$75 billion in a single quarter—was not mere luck. It resulted from laws that aligned incentives, offices that could make deals, and programs crafted to protect the public while progressing swiftly. Japan's targeted subsidies and Korea's large-scale financing demonstrate the same truth. Money is necessary, but operational models weigh even more. Industrial policy success occurs when systems adapt to challenges and continue to grow. The steps are straightforward: identify the bottlenecks, set measurable goals, assign responsibility, secure multi-year funding, hire the right talent, and make disbursement contingent on meaningful milestones. If governments do this and maintain transparency, private investment will continue, even during downturns. The next challenge will come soon. As factories launch and grids face pressure, the successful areas will be those that treat industrial policy as an ongoing process rather than a one-time effort. Focus on capacity, costs, and resilience, and the investment wave will serve as a foundation rather than a peak.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of the Swiss Institute of Artificial Intelligence (SIAI) or its affiliates.

References

Clean Investment Monitor. Q1 2025 Update. May 13, 2025. Rhodium Group & MIT CEEPR.

Milken Institute. Making a Success of Industrial Policy: Lessons and Insights from the U.S. Experience. September 2025. PDF.

NIST (U.S. Department of Commerce). "CHIPS for America has awarded over $33 billion…" News release, January 17, 2025.

OECD. "Making industrial policies work: 12 steps for smarter governance." Blog, June 25, 2025.

OECD. "Industrial policy" topic hub and related materials. 2025.

U.S. Census Bureau / FRED. Total Private Construction Spending: Manufacturing—SAAR. Latest observation July 2025.

U.S. Department of Commerce Office of Inspector General. Status Report for Commerce CHIPS Act Programs. June 2, 2025.

IEA. Global EV Outlook 2025—Electric vehicle batteries. 2025.

Japan—Reuters. "Tokyo pledges a further ¥732 billion to help TSMC expand Japan production." February 24–25, 2024.

U.S. International Trade Administration. Japan—Semiconductors (Rapidus funding overview). November 20, 2025.

Reuters. "South Korea prepares $34 billion fund for national strategic industries." March 5, 2025.

Times Union (Albany). "Palo Alto firm lands $150M to build EUV light source at Albany NanoTech; federal equity stake included." December 3, 2025.

Semiconductor Industry Association. "CHIPS supply chain investments summary." 2025.

Ethan McGowan is a Professor of AI/Finance and Legal Analytics at the Gordon School of Business, SIAI. Originally from the United Kingdom, he works at the frontier of AI applications in financial regulation and institutional strategy, advising on governance and legal frameworks for next-generation investment vehicles. McGowan plays a key role in SIAI’s expansion into global finance hubs, including oversight of the institute’s initiatives in the Middle East and its emerging hedge fund operations.