Europe's EU Innovation Gap Is Relative and Fixable

Ethan McGowan is a Professor of AI/Finance and Legal Analytics at the Gordon School of Business, SIAI. Originally from the United Kingdom, he works at the frontier of AI applications in financial regulation and institutional strategy, advising on governance and legal frameworks for next-generation investment vehicles. McGowan plays a key role in SIAI’s expansion into global finance hubs, including oversight of the institute’s initiatives in the Middle East and its emerging hedge fund operations.

Input

Modified

Europe lags by scale, not ideas: U.S. compute and China’s factories lead Gaps: late-stage capital, shared AI compute, and fast pilot manufacturing Fix: mobilize EU savings, build an AI compute commons, and speed permits and productization

The EU's innovation gap is a challenge. Still, it's also a clear opportunity for strategic action that can inspire confidence among policymakers and stakeholders. One statistic illustrates this well: as of May 2025, about three-quarters of the world's GPU cluster performance supporting AI development and implementation is in the United States. China holds around 15%. Europe is far behind. Compute power has become the new capital for innovation. Without it, great ideas struggle, and ambitious projects falter. Europe is not failing; it's outpaced by two regions driving global progress: U.S. software platforms backed by vast AI infrastructure and China's fast-paced manufacturing sector. Even though Europe launched JUPITER—the continent's first exascale supercomputer—in September 2025, the distribution of AI-grade compute remains uneven. Unless the EU matches the scale and speed of capital, compute, and commercialization, the scoreboard will remain tilted because the competition is happening on foreign turf.

Reframing the EU innovation gap

The standard narrative claims that Europe underinvests in research. This view is outdated. In 2023, EU R&D intensity reached about 2.26% of GDP, up from 2.22% the previous year. Many member states exceed 3%, and total EU R&D spending was around €381 billion in 2023. The issue isn't that Europe lacks scientific work. Instead, rivals are advancing faster in the parts of the process that now matter most for gaining market power. China's R&D growth outstripped that of the U.S. and the EU from 2024 to 2025, with Chinese total R&D spending approaching U.S. levels. The U.S. has turned its R&D into large AI platforms by concentrating compute and market resources. In contrast, Europe has a broad research base but a narrow conversion engine.

Consider instead the flow-through to scale. Private-sector risk capital in the U.S. is 6 to 8 times larger than in the EU. Even when factoring in the UK, the gap remains three to four times as large. Europe's IPO market reopened in 2024, with proceeds more than doubling from 2023; however, the absolute figures—around €14.6 billion across 57 listings—are small compared to U.S. exit markets. When capital is limited, promising firms often sell early, relocate abroad, or stall before achieving global platform status. This is not a flaw of research labs or graduates. This reflects the structure of capital markets, where depth and speed determine whether a "good" patent evolves into a "great" product on a global scale.

Capital markets, compute, and the EU innovation gap

Europe has significant savings, but they are not well utilized. Households hold around €12.1 trillion in cash and bank deposits, and an estimated €300 billion of EU savings flows abroad each year, often into U.S. markets that finance the large platforms Europe aims to compete against. The Commission's new Savings and Investments Union (SIU) seeks to connect these savings to European scale-ups, harmonize oversight, and reduce cross-border barriers. This is a correct assessment: Europe does not lack money; it lacks effective ways to direct it quickly to areas of risk. Until these pathways are improved, founders will continue to encounter early-stage support but struggle to secure late-stage funding.

The issue of computing presents another critical barrier. AI infrastructure is key in speeding up product iterations, safety testing, and market entry timelines. The U.S. accounts for most of the world's GPU cluster performance, which benefits its model builders and enterprise users. Europe's push for exascale computing is significant—JUPITER is operational, with LUMI and Leonardo also among the top ten globally—but relying on a few public supercomputers cannot replace the need for widespread, commercially available clusters. If access is limited, innovation slows; when innovation slows, time-to-market suffers. Europe requires pooled, low-friction access to AI compute for startups, universities, and small- and medium-sized enterprises (SMEs), not just for national labs.

Manufacturing scale and the EU innovation gap

China generates about 29% of global manufacturing output, nearly 12 percentage points ahead of the U.S. While Europe remains a strong manufacturing player, it operates in a world where China's scale reduces profit margins, speeds up learning, and shortens diffusion cycles. This relative scale is crucial for innovation, as manufacturing is where design meets production, and where improvements accumulate. UNIDO's 2025 data indicates that China, Europe, and North America still lead in manufacturing activity; however, Europe's recent industrial slowdowns, particularly in energy-intensive sectors, have hampered momentum and investment enthusiasm. When production moves, expertise follows, along with supply networks and feedback loops.

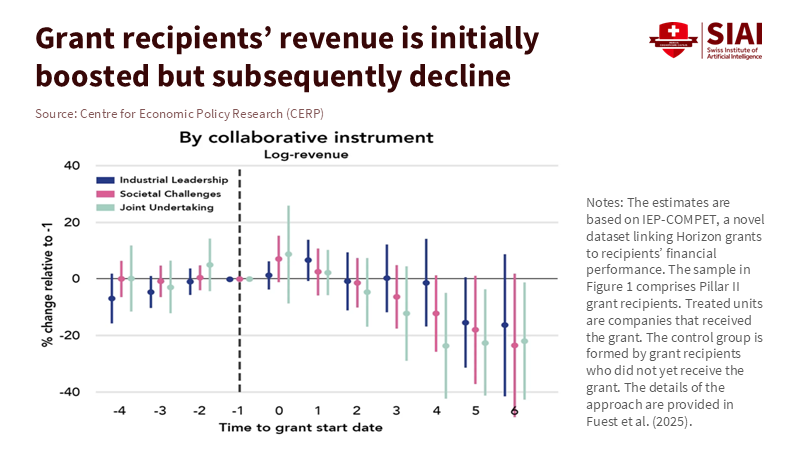

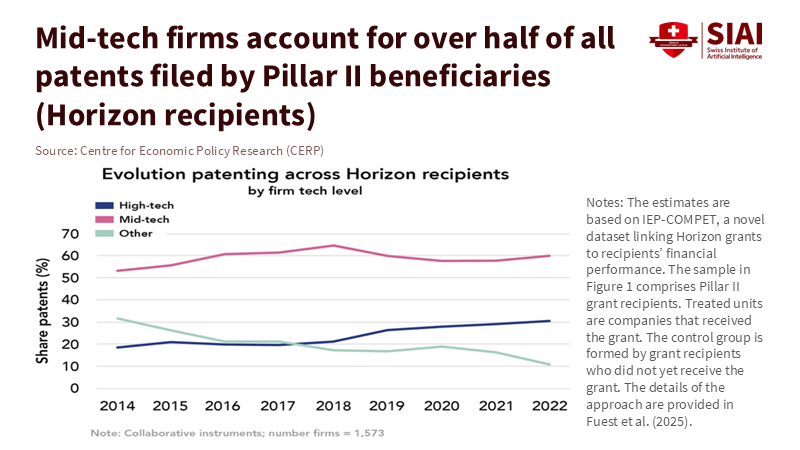

Patent data reveals a similar story. By inventor location, China leads in the number of new patents and far outpaces Europe in generative AI inventions. While quality and international presence differ, Europe maintains areas of excellence—from ASML's lithography technology to Germany's engineering expertise—but the pace of patent filings and product development is strongest where capital, compute, and factories converge. Consequently, Europe faces an increasing time-to-market gap. The research pipeline does not "break" due to a lack of ideas; it leaks where prototypes must connect with global supply chains and large-scale capital.

Closing the EU innovation gap

To address the gap, we must first recognize its relative nature. The U.S. excels in the platform phase because it combines deep reservoirs of late-stage capital with abundant AI compute and a unified exit market. China thrives in manufacturing by aligning policies, resources, supply chains, and demand at a massive scale while iterating quickly. Europe's strengths—world-class science, solid industrial niches, and common standards—can still prevail. Still, they need to be matched with systems that speed up learning from annual to weekly. This requires action in measurable areas: exits, compute, and market adoption.

First, simplify and strengthen the capital flows that support scale-ups. The SIU strategy is a step in the right direction; it should be made tangible by implementing EU-wide rules for growth listings, developing passported venture funds with quicker fund-of-funds cycles, and establishing a unified channel for venture debt to enable banks to recycle risk. A reasonable goal is to halve the U.S.–EU late-stage funding disparity by 2028. This is ambitious but achievable if a small portion of the €12.1 trillion in deposits and insurance funds gets redirected into diversified EU tech investments and if pension reforms enable longer-term contributions. Europe's IPO surge in 2024 demonstrates that there is investor interest when assets are well-packaged, and exits appear feasible. Build that credibility into the system.

Second, treat AI compute as a public-private utility, rather than just a funding line. Europe should extend the EuroHPC framework into a shared "AI compute commons" that small firms can access by the hour using straightforward credits and standard agreements—link access to open evaluation guidelines and safety audits so that usage enhances both capability and trust. Encourage national cloud leaders and global providers to place GPU clusters near universities and applied research centers, with reciprocal commitments for discounted access, internships, and shared tools. JUPITER, LUMI, and Leonardo showcase Europe's ability to create state-of-the-art resources; now, this capacity needs to be routinely available to a broader audience, not just consortia.

Third, reconnect prototypes to manufacturing. Europe cannot compete with China on volume, but it can strengthen the connection between design and pilot-line production. This involves expanding shared facilities and pilot lines for batteries, photonics, semiconductors, and biomanufacturing, as well as efficient procurement for one-of-a-kind projects in health, energy, and mobility. Use outcome-based contracts that reward learning—yield, reliability, and cost curves—not just for the number of units delivered. Horizon Europe's €93.5 billion budget should allocate larger portions to late TRL (Technology Readiness Level) sandboxes with guaranteed demand. Public purchasers should be encouraged to choose test beds over established companies when quality standards are met.

Fourth, rebuild product development around simplicity and speed. Various European studies have shown that many projects fail not due to weak science, but because teams struggle in the "valley of death" between lab potential and market readiness. The solution is straightforward: shorter cycles with real users, earlier compliance guidance, and product managers who can cut unnecessary features. National innovation agencies should link milestone grants to actual field usage and customer satisfaction targets, rather than to the volume of documentation. Universities should establish programs bringing operators into labs for extended periods. Europe's talent pool is strong, but the pace of iteration needs to improve.

Finally, streamline the approval process. The energy-intensive industry suffered after the 2022 gas crisis, and uncertainty in trade policy has undermined confidence. However, reforms in permitting, upgrades to energy grids, and expedited proceedings for clean industrial projects can help regain lost ground. Connect these initiatives to workforce training so that workers benefit from changes rather than experiencing disruptions. Simultaneously, the EU must quickly deploy its trade defense and economic security tools. Maintain strict oversight on subsidies that flood the market; keep opportunities open where reciprocity is possible and act swiftly when it is not. The goal is not to replicate others' strategies. Instead, establish a European pace that allows product teams to operate as quickly as their science permits.

One key point to remember is that the U.S. accounts for about three-quarters of global AI cluster performance. In an era focused on computing power, this advantage compounds rapidly—unless competitors disrupt the trend. Europe can accomplish this. Capital exists in our banks; about €300 billion a year is even in the region. The necessary computing resources are becoming available; JUPITER is operational, with additional capacity on the way. Science is already established here. What remains is the final step: broader exit markets, affordable access to AI infrastructure, tighter links between design and production, and a culture of rapid product development. Address these gaps, and the EU innovation gap will diminish quickly, as it is all relative. The scoreboard will change when Europe transforms the framework—by turning its savings into growth, its supercomputers into shared resources, and its prototypes into timely products. This is not just a catchy phrase; it is a realistic, achievable plan.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of the Swiss Institute of Artificial Intelligence (SIAI) or its affiliates.

References

Accel. (2024, Oct 16). AI, cloud funding in U.S., Europe, and Israel to hit $79 bln in 2024. Reuters.

ASML. (2025). 2024 Annual Report.

Dealroom & Atomico. (2023). European venture capital in 2023.

European Commission. (2025, Mar 19). Savings and Investments Union strategy (overview). European Parliament Think Tank summary.

European Commission. (n.d.). Horizon Europe funding programme (2021–2027).

EuroHPC JU / ECMWF. (2025, Sep 9). Reaching JUPITER: Europe's first exascale supercomputer.

Eurostat. (2024, Dec 11). EU spent €381.4 billion on R&D in 2023.

Eurostat. (2025, Sep 25). R&D expenditure — Statistics Explained (EU R&D intensity 2023 = 2.26% of GDP).

European Business Review. (2025, Oct 26). Why Europe's Innovation Pipeline Keeps Breaking Down.

EIB. (2024). The scale-up gap: Financial market constraints holding Europe's high-growth firms back.

FT. (2025, Nov 28). Is China winning the innovation race?

IEA. (2024). Energy and AI: energy demand from AI (regional outlook).

PwC. (2024, Dec 30). European IPO market rebounds in 2024 with proceeds more than doubling.

Statista. (2025, Apr 16). China is the world's manufacturing superpower (29% of global output in 2023).

UNIDO. (2025, Jul). World Manufacturing Production, Q1 2025 (PDF).

WIPO. (2024, Jul 3). Generative AI patent landscape: press release.

WIPO. (2024). World Intellectual Property Indicators 2024 — Patents Highlights.

Epoch AI. (2025, Jun 5). AI supercomputers performance share by country (U.S. ~75%, China ~15%).

Reuters. (2025, Dec 2). EU takes small steps in uphill struggle to wean savers off cash (cash/deposits €12.1 trn; ~€300 bn outflow yearly).

Reuters. (2025, Dec 4). EU plans to overcome investment hurdles hampering competitiveness (SIU proposals).

Ethan McGowan is a Professor of AI/Finance and Legal Analytics at the Gordon School of Business, SIAI. Originally from the United Kingdom, he works at the frontier of AI applications in financial regulation and institutional strategy, advising on governance and legal frameworks for next-generation investment vehicles. McGowan plays a key role in SIAI’s expansion into global finance hubs, including oversight of the institute’s initiatives in the Middle East and its emerging hedge fund operations.