The Hidden Fiscal Shock of Climate Change: Why Public Budgets, Not Temperatures, Are the Real Crisis

Erik Van der Meer examines how scientific knowledge is produced, validated, and institutionalized across disciplines. His writing explores the structure of modern science, the evolution of research norms, and the interaction between technology and scientific epistemology. He contributes reflective essays on science itself—bridging hard research and meta-level analysis.

Input

Modified

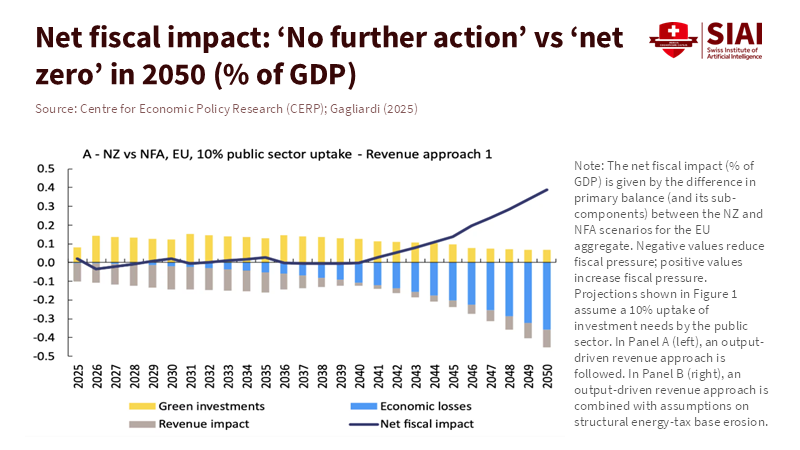

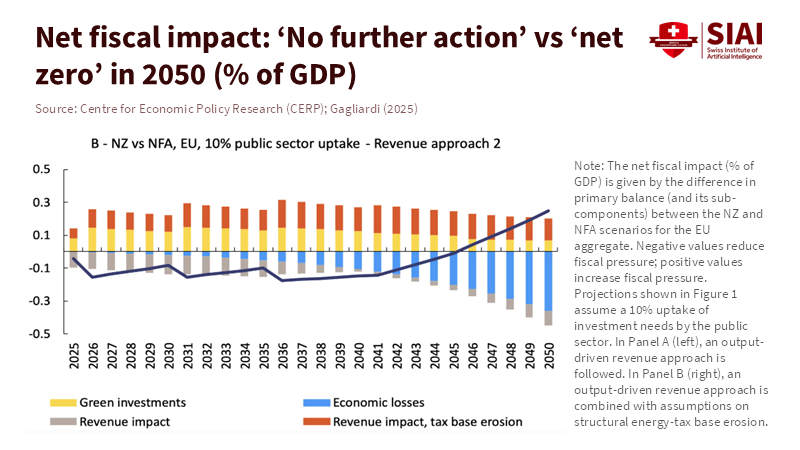

Climate shocks now directly strain public budgets and weaken tax bases Disaster spending and insurance gaps are becoming fiscal risks Without EU coordination, climate risk turns into a lasting deficit

The most revealing number in Europe’s climate debate is not a degree of warming. It is a budget line. Over the past decade, European governments have quietly shifted tens of billions of euros each year toward emergency relief, reconstruction, and insurance backstops linked to climate disasters. In recent years, public disaster spending in the EU has exceeded annual spending on entire education sub-sectors. This statistic reframes the climate question. Climate change is not primarily a story about discomfort, heat, or even environmental loss. It is a story about fiscal shock. When floods, fires, and heatwaves occur, governments are expected to intervene. They always do. The money comes from current budgets, future debt, or foregone investment elsewhere. At the same time, local tax bases shrink as firms close, workers relocate, and insured losses go unpaid. Climate change, in other words, is not a marginal issue layered onto public finance. It is already changing how states raise money, spend it, and justify trade-offs. This matters now because the fiscal strain is compounding faster than policy systems are adapting. The focus keyword in this analysis is climate change public finance, and the evidence indicates that it should be central to education and policy debates.

Climate Change, Public Finance, and the Illusion of Manageable Damage

The dominant misunderstanding about public finance for climate change is the belief that damages are small, local, and temporary. A heatwave passes. A flood recedes. Life resumes. From this view, higher temperatures mean higher tolerance thresholds. But public finance does not work on tolerance. It works on exposure and obligation. When climate disasters occur, European governments confront immediate and unavoidable fiscal duties: emergency services, housing support, infrastructure repair, and business relief. These are not optional expenditures. They are politically and legally embedded expectations. Between 2021 and 2024, Europe experienced a sequence of floods, droughts, and wildfires that repeatedly triggered national emergency mechanisms and EU-level solidarity funds. Annual public spending linked to climate disasters has risen structurally above levels in the early 2000s, even after inflation adjustment. This trend matters more than the exact temperature increase because budgets respond to events, not averages.

The second illusion is that insurance absorbs most of the shock. In reality, Europe encounters a significant and persistent insurance protection gap. In several member states, less than half of climate-related losses are insured. When insurance coverage is absent or withdrawn, governments become the insurer of last resort. Public compensation schemes, ad hoc relief packages, and tax deferrals fill the gap. This directly links public finance for climate change to future fiscal capacity. Every euro spent on reconstruction without prior risk pricing is a euro not spent on education, research, or skills. The fiscal problem deepens because these expenditures are volatile and correlated. A single disaster can push local or national budgets off course for years, especially in regions with narrow tax bases.

What makes this moment different is accumulation. Climate shocks are no longer rare enough to be smoothed over time. They arrive before budgets recover from the previous event. The result is fiscal layering: emergency spending piled on top of already-constrained public finances. This undermines medium-term planning and weakens credibility with investors and insurers. Climate change public finance is therefore not about future risk. It concerns the current instability that erodes the foundations of public investment.

Climate Change, Public Finance, and the Decline of the Tax Base

Public finance depends on predictability. Climate change undermines that predictability at its source: the tax base. After a major climate shock, affected regions frequently see prolonged declines in business activity, employment, and property values. Firms shut down or relocate. Workers migrate. Tourism declines. These effects reduce income, corporate, and consumption tax revenues for several years. Empirical studies using post-disaster regional data in Europe show that local tax revenues can remain depressed well beyond the initial reconstruction phase. This is a critical yet underappreciated channel in climate-change public finance.

The feedback loop is simple. Climate disaster strikes. Government spending rises sharply. Conversely, revenue declines. The fiscal gap widens from both sides. To close it, governments borrow, cut other spending, or raise taxes elsewhere. Each option has distributional and political costs. Borrowing increases debt service. Spending cuts often hit long-term investments, including education and training. Tax increases can slow recovery. None of these outcomes is a temporary inconvenience. They form public budgets for a decade or more.

This pattern also exposes regional inequality. Wealthier regions are better insured and recover more quickly, thereby preserving their tax base. Poorer or marginal regions rely more heavily on public support and recover slowly. Climate change public finance thus becomes a driver of territorial divergence within the EU. This has immediate implications for education systems. Regions with shrinking fiscal capacity struggle to maintain school quality, teacher pay, and adult training programs, just as climate adaptation demands new skills. The price of inaction is not only higher disaster-related costs but also weaker human capital formation over time.

Critics sometimes claim that these effects are overstated because economies are resilient. Resilience, however, is uneven and conditional. It depends on insurance availability, fiscal space, and governance capacity. Where these are lacking, climate shocks leave permanent scars. Climate change public finance must therefore be understood as a structural issue rather than a cyclical one. Ignoring the tax base channel leads to systematic underestimation of long-term costs.

Climate Change Public Finance, Insurance Retreat, and Systemic Risk

Insurance markets are an early-warning system for public finance in the context of climate change. When insurers raise premiums, limit coverage, or exit high-risk regions, they are pricing risks that public budgets will soon absorb. Across Europe, climate-related insurance premiums have risen sharply since the early 2020s, and coverage has become more restrictive in flood- and fire-prone areas. In some cases, private insurance has effectively withdrawn, leaving households and firms exposed. Governments respond by increasing public insurance schemes or offering post-disaster compensation. This shifts risk from private to public balance sheets.

The fiscal implication is systemic. As climate risks increase, public contingent liabilities increase accordingly. These liabilities rarely appear in headline debt figures, but they shape expectations. Financial markets increasingly price sovereign risk based on exposure to climate shocks and the credibility of fiscal responses. Climate change public finance, therefore, intersects with financial soundness. A large disaster can simultaneously increase public spending needs, reduce revenues, and raise borrowing costs. This triple effect is challenging to manage, especially for highly indebted countries.

There is also a coordination problem at the EU level. Climate risks do not respect borders, but fiscal responses remain largely national. Solidarity mechanisms exist, yet they are limited in scale and slow to deploy. The recent breakdowns in international climate negotiations highlight a deeper issue: failures of united action translate into fiscal vulnerability. For the EU, climate change public finance is a diplomatic issue as much as a domestic one. Without coordinated funding strategies and risk-sharing mechanisms, member states face fragmented and inefficient responses.

Some argue that increasing public insurance crowds out private markets. The evidence suggests the opposite. Clear public frameworks might stabilize expectations and encourage private participation. What undermines markets is uncertainty and ad hoc intervention. A transparent approach to public finance for climate change, with pre-funded adaptation and risk pooling, reduces the need for emergency bailouts. The alternative is a reactive system that amplifies fiscal shocks.

Climate Change Public Finance as an Education and Policy Imperative

Education policy rarely enters climate finance debates, yet it should. Climate change public finance directly affects education budgets through competition for resources. Emergency spending displaces long-term investment. When governments encounter repeated fiscal shocks, education becomes a silent casualty. Teacher shortages worsen. Infrastructure renovations are delayed. Lifelong learning programs are being cut just as labor markets demand new skills to adjust and mitigate. This is not a remote risk. It is already visible inside regions repeatedly hit by climate events.

Reframing climate change public finance as an education issue clarifies the stakes. Adaptation is not only about seawalls and drainage. It is about skills, planning, and institutional capacity. These are built through education systems that require stable funding—policymakers who treat climate spending as exceptional miss this link. The more original approach is integration. Climate risk should be embedded in fiscal planning, insurance regulation, and education investment strategies. This reduces volatility and preserves human capital.

A common critique is that fiscal resources are limited and priorities must be ranked. That is precisely why public finance for climate change matters. Ignoring it does not save money. It defers costs until they are larger and more disruptive. Evidence from recent European disasters shows that ex post spending is consistently higher than preventive investment would have been. The method is simple: compare reconstruction costs with estimated adaptation costs using standard public investment appraisal. The gap is large and persistent.

The call to respond is not abstract. Governments should treat climate risk as a core fiscal variable, alongside aging and debt. Education leaders should engage in these debates, not as advocates for their own budgets, but as stewards of long-term capacity. Climate change public finance is the bridge between environmental risk and social resilience. Crossing it requires abandoning the illusion that a warmer world is merely uncomfortable. It is fiscally transformative.

The opening statistic bears repeating: climate change appears first and most prominently in public budgets. Degrees of warming do not bankrupt states. Repeated, underpriced fiscal shocks do. Europe’s experience over the past decade makes this clear. Emergency spending is rising. Insurance is retreating. Tax bases are eroding in at-risk areas. Together, these trends redefine climate change public finance as a central policy challenge rather than a peripheral concern. The choice is stark. Continue to treat climate disasters as exceptional events and absorb escalating fiscal damage, or integrate climate risk into fiscal planning, insurance schemes, and education investment now. The second path appears more expensive, but it is actually cheaper. It preserves public capacity, stabilizes expectations, and protects the institutions that uphold growth and learning. Climate change is no longer a future scenario. It is a present fiscal condition. Recognizing that fact is the first step toward governing it.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of the Swiss Institute of Artificial Intelligence (SIAI) or its affiliates.

References

Centre for Economic Policy Research (CEPR). Europe’s public finances in a warming world. CEPR Policy Portal (VoxEU), London.

European Commission. Annual reports on the European Union Solidarity Fund. Publications Office of the European Union, Brussels.

European Environment Agency. Economic losses and fatalities from weather- and climate-related extremes in Europe. EEA Report Series, Copenhagen.

Geneva Association. The climate change insurance protection gap: Why it matters and how to reduce it. Geneva.

Organisation for Economic Co-operation and Development (OECD). Climate adaptation and fiscal resilience: Managing public finance risks. OECD Publishing, Paris.

Reuters. EU rethinks climate diplomacy after bruising COP30 summit, internal document shows. Reuters Sustainability and Climate Desk.

SUERF – The European Money and Finance Forum. Is Europe adapting to a changing climate? Part III: Financing needs, gaps, and insurance protection. SUERF Policy Notes and Briefs.

Erik Van der Meer examines how scientific knowledge is produced, validated, and institutionalized across disciplines. His writing explores the structure of modern science, the evolution of research norms, and the interaction between technology and scientific epistemology. He contributes reflective essays on science itself—bridging hard research and meta-level analysis.