Incentives, Not Ideology, Will Decide the Dollar–Renminbi Digital Race

His recent work examines the broader socioeconomic consequences of artificial intelligence, including labor markets, public finance, demographic change, institutional adaptation, and the distributional effects of technological progress.

He holds a PhD in Mathematical Finance from Boston University, and previously earned an MSc in Finance and Economics from the London School of Economics. He completed his undergraduate studies in Economics at Seoul National University under the Korea Foundation for Advanced Studies scholarship program.

Input

Modified

Incentives, not ideology, will decide the dollar–RMB digital race Regulated dollar stablecoins scale; e-CNY stays domestic as China tests HK yuan stablecoins Regulate tightly and pilot cross-border payments in education and trade—measure, don’t mandate

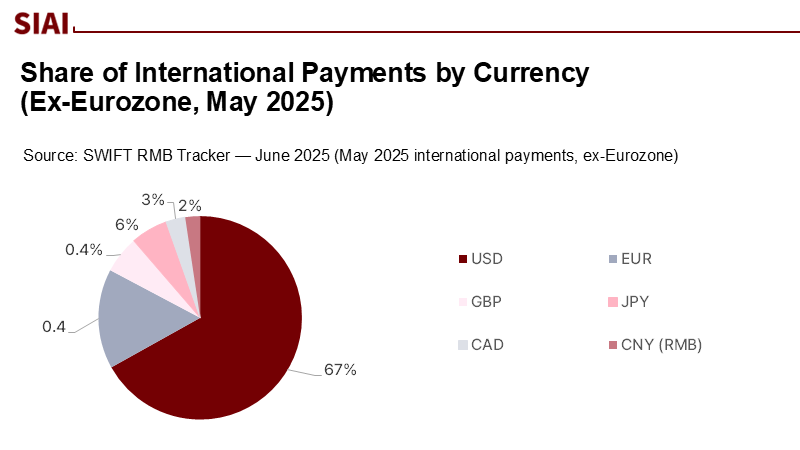

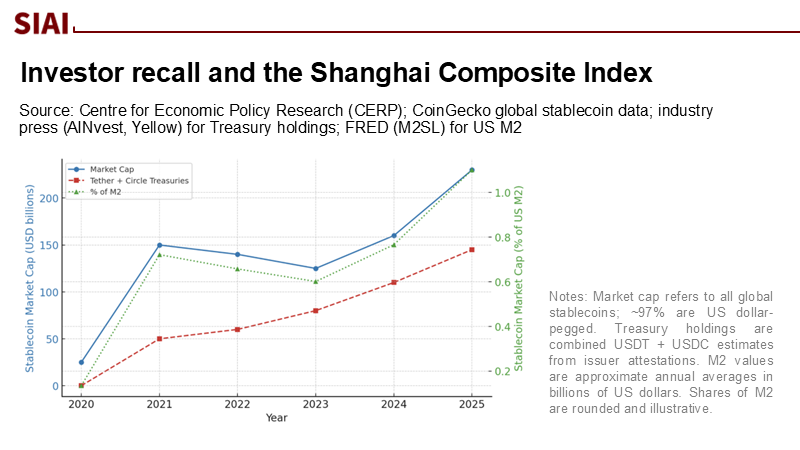

A single private issuer of “digital dollars,” Tether, disclosed $127 billion in U.S. Treasury bills on its balance sheet this summer—more than the holdings of several G20 sovereigns. That is not a crypto curiosity; it is a blunt signal about incentives. Stablecoins have become a yield-powered distribution mechanism for the dollar, routing cash into safe assets while providing users with instant, 24/7 settlement. By contrast, China’s central-bank digital currency (e-CNY) has processed trillions of yuan in domestic transactions but has not lifted the renminbi’s share of global payments above ~2.9%. The market, in short, is rewarding a model where private actors can profit by serving users quickly at scale; it is not yet satisfying a state-led model that lacks cross-border acceptance and profit-aligned champions. The contest between U.S. dollar stablecoins and China’s CBDC will therefore turn on incentive design, not just technology. Today, the incentives clearly favor stablecoins.

What the Currency Race Really Tests

The digital-currency debate is usually framed as a technology arms race: central banks build CBDCs, startups mint tokens, and the fastest chain wins. That frame is misleading. The actual test is monetary discipline under decentralized distribution. Stablecoins promise one-to-one redemption against cash or Treasuries; to maintain that promise at scale, issuers must keep pristine reserves and real-time transparency. This incentive—survival through credibility—has been sharpened in the United States by the GENIUS Act of July 2025, which federalizes reserve, redemption, and supervision standards for payment stablecoins. The Act’s clarity signals to banks, payment networks, and merchants that these instruments can be integrated into the existing financial system without requiring them to guess the rules. Policy did not invent demand; it aligned with it. The result is rising institutional adoption built on compliance and yield.

Meanwhile, Beijing’s approach has been the mirror image: build a high-capacity CBDC first, manage it tightly at home, and extend it abroad through official corridors. The e-CNY pilot is indeed massive by any traditional metric—encompassing multi-trillion-yuan cumulative transactions across numerous provinces. However, cross-border is where currency competition matters, and here technology runs up against policy walls. The renminbi’s global payment share remains stuck at around 2.9%, a reminder that capital controls and convertibility, rather than front-end efficiency, set the ceiling for international usage. Even promising multi-CBDC efforts, like Project mBridge—which is now at a minimum viable product stage—cannot substitute for profound, permissionless network effects. Unless non-Chinese firms and households want to hold and use the unit, the rails will run half-empty.

Stablecoins vs CBDCs: The Incentive Divide

By the numbers, the private rails are pulling ahead. Dollar-pegged stablecoins now account for the overwhelming majority of a market that has climbed past $250 billion to $280 billion in capitalization; USDT and USDC alone exceed $210 billion, and on several measures, they have processed trillions in on-chain settlements over the past year. Those balances are primarily invested in short-dated U.S. Treasuries, embedding a feedback loop: the more users demand digital dollars, the more Treasury demand rises, reinforcing the dollar’s primacy. These facts do not settle the policy debate—but they do reveal why the “American-style” strategy of regulated private money on public rails is scaling faster than state-issued designs, indicating a shift in the balance of power in the digital currency market.

Crucially, recent U.S. legislation did not merely bless stablecoins; it tightened constraints. The GENIUS Act restricts interest-bearing features and codifies reserve quality, redemption rights, and supervision. Bank lobbyists already fret about deposit flight if platforms can wrap yield around stablecoins, which underscores the point: competition discipline is doing work that policy alone cannot. When issuers profit only if their tokens hold par, their incentives line up with user safety; when they chase growth with weak backing, redemption runs punish them. The Bank for International Settlements has warned about run and fire-sale risks if the sector continues to balloon—again, an argument for bank-grade rules rather than a wholesale retreat. The policy task is to contain tail risks without smothering the incentive to serve users.

There is a human, not just macro, dimension here. Cross-border payments remain costly and slow for families and students. The global average remittance cost for sending $200 remains ~6.5%, and while fintechs have reduced fees, progress has stalled in specific corridors. In parallel, university bursars grapple with expensive and opaque international tuition flows, even as cross-border education becomes a larger economic line item—UK institutions derived approximately £12.1 billion (≈$16.0 billion USD) (≈23%) of their income from international students in 2023/24. Properly regulated stablecoins—settling near-instantly at low network cost and redeemable at par—offer a glimmer of hope, targeting frictions that CBDCs, aimed at domestic policy transmission, were not designed to fix. For educators and administrators, the benefits are practical: cheaper refunds, fewer chargebacks, cleaner reconciliation, and improved visibility, providing a sense of relief and reassurance.

China’s Dual Gamble, America’s Market Bet

Beijing appears to recognize the incentive mismatch. Credible reporting suggests that China is considering yuan-backed stablecoins to promote the global adoption of the RMB—a significant shift from the 2021 crypto ban. The venue for that experiment is obvious: Hong Kong, whose Stablecoins Ordinance took effect August 1, 2025, creating a licensing regime for fiat-referenced issuers under the HKMA, complete with reserve, redemption, disclosure, and AML rules. In other words, China is preparing a dual-rail strategy: to keep the CBDC as a programmable domestic instrument and to test licensed, HK-based stablecoins as the offshore conduit, aligned with market demand for dollar-like liquidity. This dual-rail strategy is a significant shift in China's approach to digital currencies, indicating a more nuanced understanding of market dynamics and user needs.

The logic is straightforward. Hong Kong already clears the bulk of offshore RMB. He sits atop the USD-pegged HKD currency board, making it uniquely suited to intermediate between e-CNY corridors and dollar liquidity. Suppose regulators license a small number of bank-grade HKD or CNH-referenced stablecoins with daily reserve disclosure and instant redemption at par. In that case, they can meet global users where they are—on stablecoin rails—while ring-fencing mainland monetary control. BIS’s warnings about stablecoin “singleness,” elasticity, and integrity still apply; yet those concerns are precisely what licensing, reserve quality, and circuit-breakers are meant to address. The aim is not to make stablecoins sovereign; it is to make them supervised, so they can shoulder real trade and treasury work without amplifying systemic risk.

A realistic way to think about scope is through scenario math. Suppose just 3% of China’s 2024 exports (~$3.58 trillion) shift to HK-licensed stablecoin settlement by 2027 via trade financiers and large corporates. That would channel roughly $107 billion annually through supervised rails—not enough to breach capital controls, but sufficient to enhance liquidity, solidify operational processes, and generate market data on costs, speed, and compliance outcomes. That estimate is intentionally conservative—method: 0.03 × $3.58 trillion—and it keeps the focus on learning under constraints rather than on headline-grabbing leaps. What matters is that incentives are aligned: exporters want speed and fewer FX frictions; Hong Kong wants to anchor its role as a regulated digital-asset hub; Beijing wants control at home and influence offshore.

For the education sector, the dual-rail experiment could be tangible within planning cycles. Student flows are growing toward ~6.9 million internationally mobile learners, and cross-border tuition platforms already process billions in quarterly volume. If HK-licensed stablecoins interoperate with tokenized deposits and CBDC corridors, bursar offices could receive funds in minutes with deterministic settlement and automated compliance checks, while preserving the option to convert into insured deposits immediately. The policy prerequisite is not ideological buy-in; it is clear counterparty rules. Universities and ministries should pilot controlled use cases, such as tuition refunds, scholarship disbursements, or research grant transfers, with embedded reporting. The benefits—lower costs, fewer errors, and increased visibility—align directly with sector sustainability at a time when margins are tightening.

Skeptics will counter that stablecoins threaten monetary sovereignty and can accelerate capital flight or sanction evasion. These concerns are legitimate and must be addressed. First, licensing in Hong Kong establishes ex ante guardrails (reserve composition, redemption windows, audit cadence) that reduce run externalities. Second, use-case gating—starting with B2B trade finance, escrow, or wholesale settlement—limits retail speculation and surfaces compliance telemetry early. Third, the CBDC/mBridge stack handles public-sector and interbank flows where state objectives dominate, preserving policy levers. Finally, the U.S. framework demonstrates how to channel private incentives into public goods: by making reserves safe and redemptions real, the system harnesses profit motives for currency distribution without surrendering oversight. The contest then becomes not “state vs market,” but which jurisdiction best fuses them.

Incentives Will Choose the Winner

The Call Is to Align, Not Impose. We began with a startling statistic: a private stablecoin issuer sitting on $127 billion in T-bills because users want instant, programmable dollars. That gravitational field—not rhetoric—explains why dollar-stablecoins are attracting global liquidity and why CBDCs without cross-border acceptance remain domestic tools. China’s dual gamble—CBDC at home, HK-licensed stablecoins offshore—acknowledges this reality. The United States, by federalizing stablecoin rules, has bet that disciplined private money can fortify rather than fragment the dollar system. Education leaders, administrators, and policymakers should respond in kind: pilot narrowly, measure ruthlessly, regulate transparently. Design incentives so that the people moving value—students paying tuition, universities issuing refunds, firms shipping goods—benefit first. The winner of this race will not be the flashiest technology or the boldest press release. It will be the architecture that enables users to help themselves—safely, affordably, and at scale.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of the Swiss Institute of Artificial Intelligence (SIAI) or its affiliates.

References

Atlantic Council. CBDC Tracker (updated 2024–2025).

Bank for International Settlements (BIS). Annual Economic Report 2025, Chapter III: The next-generation monetary and financial system (June 24, 2025).

BIS. Project mBridge reaches MVP stage (updated November 11, 2024).

BIS. Stablecoin growth – policy challenges and approaches (BIS Bulletin No.108, July 11 2025).

Davis Polk. Hong Kong’s new stablecoin licensing and regulatory regime (July 8, 2025).

DefiLlama. Stablecoins – Total Market Capitalization (accessed Aug 2025).

Flywire. Q2 2025 Financial Results (August 5, 2025).

HKMA. Regulatory Regime for Stablecoin Issuers (effective August 1, 2025).

IMF. Crypto-Assets Monitor (May 23, 2025).

Mayer Brown. GENIUS Act Signed into Law: U.S. Enacts Federal Stablecoin Legislation (July 18, 2025).

Reuters. Exclusive: China considering yuan-backed stablecoins to boost global currency usage (August 21, 2025).

SCMP. In 2024, exports grew to US$3.58 3.58tn (January 13, 2025).

SWIFT. RMB Tracker – June 2025 (June/July 2025).

Tether. Q2 2025 Attestation: U.S. Treasury holdings ~$127bn (July 31, 2025).

The Block. Stablecoin market capitalization surpasses $250 billion (June 2, 2025).

UK House of Commons Library. International students in UK higher education (June 27, 2025).

World Bank. Remittance Prices Worldwide – Issue 53, March 2025 (Q1 2025).

His recent work examines the broader socioeconomic consequences of artificial intelligence, including labor markets, public finance, demographic change, institutional adaptation, and the distributional effects of technological progress.

He holds a PhD in Mathematical Finance from Boston University, and previously earned an MSc in Finance and Economics from the London School of Economics. He completed his undergraduate studies in Economics at Seoul National University under the Korea Foundation for Advanced Studies scholarship program.