BRI Dependency Risk Is Rewiring Global Value Chains

His recent work examines the broader socioeconomic consequences of artificial intelligence, including labor markets, public finance, demographic change, institutional adaptation, and the distributional effects of technological progress.

He holds a PhD in Mathematical Finance from Boston University, and previously earned an MSc in Finance and Economics from the London School of Economics. He completed his undergraduate studies in Economics at Seoul National University under the Korea Foundation for Advanced Studies scholarship program.

Input

Modified

BRI is reshaping value chains, creating real growth with tight dependencies U.S. aid retrenchment weakens competition and deepens China-centric standards Build resilience: fund vendor-neutral training and multi-standard curricula in every deal

On a winter morning in 2025, two numbers changed the landscape of development. Washington revealed that 83% of USAID programs were cut after a six-week review. At the same time, Beijing’s global builders announced record Belt and Road (BRI) deal volumes in the first half of the year. These developments occurred mere months apart and conveyed a clear message. The competition to fund infrastructure and shape value chains shifted from a tug-of-war to a one-sided pull. This change impacts schools and labs just as much as it does ports and power plants. When aid disappears and investment flows in from a single source, skills, curricula, and hiring gravitate toward that source. This is the essence of BRI dependency risk. Ignoring it means we hand over the next decade of talent development to whoever finances the infrastructure projects. These numbers are tangible; they determine how countries learn, produce, and trade.

BRI Dependency Risk in Value Chain Shifts

BRI started with complex infrastructure and has evolved into a platform for controlling supply chains. Indonesia illustrates what rapid industrialization can look like when built on a single set of partnerships. Chinese companies control about three-quarters of Indonesia’s nickel-refining capacity, which is crucial to electric vehicles. Indonesia produced 51% of the world’s mined nickel in 2023. This output supplies Chinese-backed smelter parks and downstream battery materials. The industrial base is substantial, yet it also reveals a dependence on one network of investors, technology, and buyers. When prices fluctuate, labor standards tighten, or export regulations shift, policymakers have less room to maneuver. This situation is a real example of dependency risk. It ties local skill development to decisions made far from the ministries and universities of the host country.

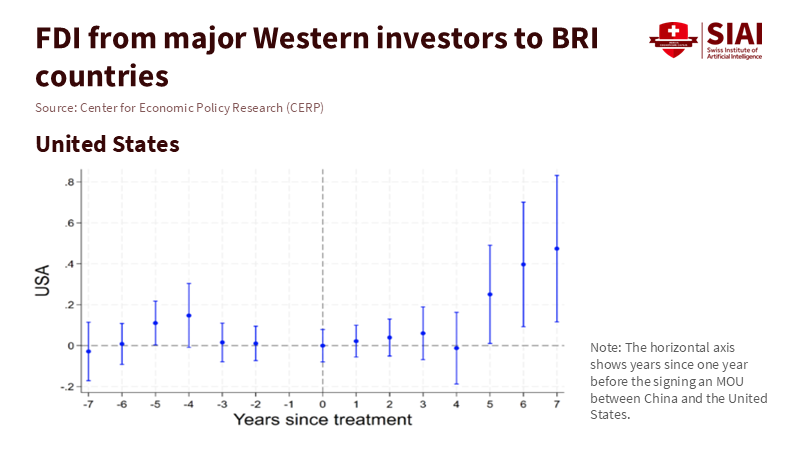

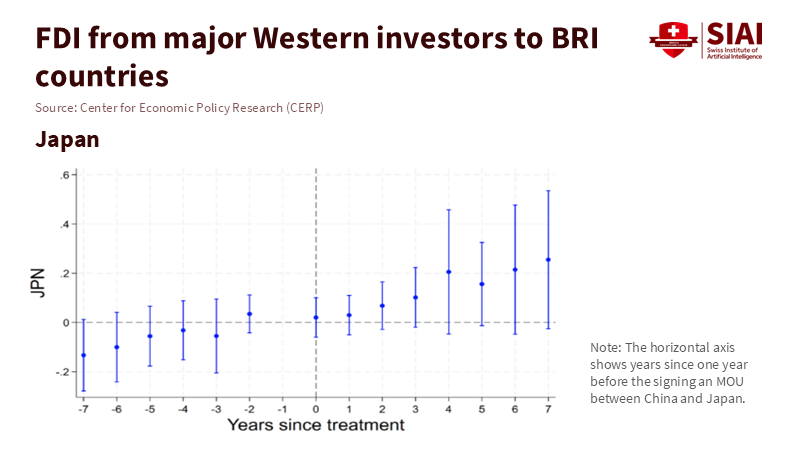

This trend is not limited to Southeast Asia. Europe now houses some of the most significant Chinese battery investments outside of China. Hungary leads the continent in attracting Chinese electric vehicle and battery projects, backed by a €7.3 billion plant in Debrecen. Morocco has positioned itself as a bridge between Europe and Africa for electric vehicle supply chains. Chinese battery manufacturers have committed to multibillion-dollar factories there, taking advantage of Morocco’s automotive export base and its trade links with the EU and the United States. These investments promise jobs, vendor ecosystems, and technology spillovers. However, they also deepen dependence on a single set of standards, logistical choices, and component sources. Any disruption in inputs or financing from China could affect training programs, vocational curricula, and apprenticeships in Hungary and Morocco. The education sector cannot work in isolation; it must address the BRI dependency risk embedded in these value chains.

BRI Dependency Risk and Competing Finance

For a decade, rival financing has helped mitigate dependency. The U.S. Development Finance Corporation set records in 2024, committing $12 billion across food, energy, health, and critical infrastructure. The U.K.’s British International Investment increased its commitments significantly in 2024, particularly in Africa. Japan continued to allocate over half of its bilateral ODA to economic infrastructure, with a heavy focus on transport and energy. This competition didn’t always match BRI’s speed or scale, but it was significant. It provided borrowing countries with options and leverage. It also diversified the technical standards present in classrooms and technical colleges, from grid codes to train maintenance.

That balance shifted in early 2025. Reuters and the Associated Press reported that the Washington administration cut about 83% of USAID programs following a quick review. A European Parliament briefing called this move a dismantling of the agency. Independent trackers noted a freeze and rescission push. Regardless of the final legal outcome, the immediate effect was a significant drop in the U.S. grant-based development presence. At the same time, Chinese BRI activities reached new heights, contributing to a substantial overseas development and construction footprint measured in hundreds of billions. Competition persists, but the playing field has changed. The risk is not about one country “winning.” Instead, it’s about borrowing nations losing their ability to negotiate and their education systems failing to receive the diverse standards and partnerships that strong learning ecosystems require.

BRI Dependency Risk in Practice: Case Evidence

Transport corridors reshape both trade and training. The China–Laos Railway exemplifies this. Freight volumes have reached new highs each year since its opening, moving about 19.6 million tons in 2024 and more than 70 million tons cumulatively by late 2025. Exports to China from Laos increased at double-digit rates. Logistics programs in Vientiane are now training students for cross-border rail operations using Chinese systems and standards. This brings jobs and skills but also creates technical dependencies—from signaling software to spare parts—that local colleges must continually source from a single supplier ecosystem. Breaking this dependence becomes costly once the curriculum and vendor base are entrenched around one standard.

Energy corridors illustrate a similar situation. Pakistan’s power sector added significant capacity under the China-Pakistan Economic Corridor (CPEC). The country addressed urgent demand, but at a cost. Capacity payments surged to record levels, straining the budget and squeezing social spending, including education. Circular debt increased. When grants and concessional financing lessened, renegotiating terms became more difficult, putting pressure on tariffs and cuts. While training centers expanded technician programs for new plants, they struggled to fund STEM labs and hire teachers when capacity charges consumed their budgets. Dependency risk directly impacts education just as much as it does trade data.

Reducing BRI Dependency Risk: A Policy Playbook

The lesson isn’t to reject BRI financing but rather to create options that lower exposure to any single network. First, shift from project-by-project training to sector-wide human-capital partnerships. When countries negotiate rail or battery agreements, they should secure multi-year funding for local universities and technical colleges that is vendor-neutral and open in curriculum. This means specifying budget allocations for faculty development, laboratories, and dual-certification programs that align with Chinese, European, and international standards. It also requires explicit commitments to local research in maintenance, compliance, and safety areas that are often underfunded in fast-tracked projects. New BRI data show a trend toward equity stakes and partnerships rather than pure sovereign loans, creating opportunities to exchange small equity stakes for long-term training endowments that withstand market fluctuations.

Second, revive and refocus competing finance. The DFC’s commitments in 2024 and BII’s ramp-up show a foundation to build upon. Japan’s ODA profile indicates ongoing strength in quality infrastructure. The gap lies in grants and technical assistance after USAID’s cuts. This gap can partially be filled with coalition tools: the G7’s Partnership for Global Infrastructure and Investment and various trilateral agreements that connect DFC, JBIC, and European agencies to speed project preparation. Governments in borrowing nations should also create “standard-agnostic” curricula that teach students to operate Chinese systems while ensuring equivalency with EU and IEC standards. This requires funding, but not on the scale of a power plant. It involves careful procurement and a commitment to bundling learning obligations into every port, grid, and rail contract. In short, reduce BRI dependency risk by building redundancy in skills and standards rather than seeking an ideal counterweight that may not arrive soon.

Anticipating the Pushback

Three common criticisms arise. The first is that BRI is winding down, so dependency will lessen. China’s new sovereign lending indeed turned negative in recent years as repayments exceeded new loans. Beijing has also spent the last three years restructuring tens of billions in distressed debt and shifting from direct project financing to more equity investments and support through development banks. However, a slowdown in one channel has been offset by increases in construction contracts and equity-style investments, particularly in energy and metals. Dependency risk changes form but does not disappear.

The second critique claims competition remains strong even without USAID. DFC, BII, and JICA are still active, which is accurate and positive. However, grants and technical programs serve a unique role that commercial lenders cannot fill. They support curriculum development, teacher training, safety oversight, and environmental labs—the essential “software” that keeps infrastructure safe and efficient. When this layer is removed, countries rely more on vendor-provided training, which inevitably narrows their exposure to standards and weakens their bargaining power. The solution is not to yearn for past aid models but to create targeted grant windows funded collaboratively across allied nations, accompanying large loans and equity.

The third criticism states that BRI influences countries only through investment returns, not policymaking power. The evidence is mixed. Debt restructurings since 2020 have seen China work alongside Paris Club creditors and the IMF, as in the case of Zambia, and often on reasonable terms. This challenges simplistic “debt trap” narratives. However, influence doesn’t necessarily mean coercion. It can arise from standard-setting, procurement systems, and local training dependencies. When one vendor dominates a sector, switching becomes costly for both governments and educators. This is a form of soft lock-in that shapes decisions for years to come. The sensible response is not alarmism but rather diversification, transparency about long-term operating costs, and investment in educational capacity that endures beyond individual projects.

We started with two numbers from early 2025: an 83% drop in USAID programs and a record increase in BRI activities. Together, they define the BRI dependency risk for the coming decade. Value chains will continue to shift towards areas that can support battery parks, rail hubs, and energy corridors. This is promising if countries can leverage it to create jobs and improve education. It becomes risky if a single network controls the standards, systems, and parts that keep these systems operational. The answer isn’t to wait for a geopolitical change. It is to include learning and standard diversity in every agreement we sign this year. Universities and ministries must see skills development as essential infrastructure, not an afterthought. Lenders should tie funding to vendor-neutral training and international safety certifications. Legislatures ought to require transparent reporting on long-term costs that impact education budgets. If we implement these straightforward actions, those two numbers won’t dictate our future but rather help guide our choices. That’s how we can exert our agency in a world shaped by the BRI and the gaps left by others.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of the Swiss Institute of Artificial Intelligence (SIAI) or its affiliates.

References

AidData. (2024, March 26). The BRI at 10: A report card from the Global South

AidData. (2025). Belt and Road Reboot: Executive summary.

Associated Press. (2025, March 10). Secretary of State Rubio says purge of USAID programs complete, with 83% of agency’s programs gone.

Boston University Global Development Policy Center. (2025, October 10). Developing nations rack up $3.9 billion in net debt payments to China a year. https://www.reuters.com/ (report coverage)

British International Investment. (2025, July 4). Annual Review 2024: £1.75 billion of commitments.

C4ADS. (2025, February 5). Chinese firms control around 75% of Indonesian nickel capacity, a report finds. https://www.reuters.com/ (report coverage)

Carnegie Endowment for International Peace. (2023, April 11). How Indonesia used Chinese industrial investments to turn nickel into the new gold.

DFC—U.S. International Development Finance Corporation. (2024, October 24). Record $12 billion in investments in FY 2024.

Financial Times. (2025, July). BRI investment and construction activity hits record in H1 2025.

Green Finance & Development Center. (2025, July 17). BRI investment report 2025 H1.

IEEFA. (2024, October 24). Indonesia’s nickel companies need renewable energy amid increasing production.

Japan—OECD Development Co-operation Profiles. (2025, June 11). Japan.

KFF. (2025). U.S. foreign aid freeze & dissolution of USAID: Timeline of events.

Reuters. (2024, August 29). China’s lending to Africa rises for first time in seven years.

Reuters. (2024, June 6). Gotion High-Tech to build EV battery gigafactory in Morocco.

Rhodium Group. (2023, June 29). China’s external debt renegotiations after Zambia.

U.K. Africa Global Funds. (2025, July 8). BII boosts African investments by 40%.

World Bank. (2019). Belt and Road Initiative: Brief.

Xinhua / China–Laos railway updates. (2025, November 2). Freight volume surpasses 70 million tons.

Xinhua / Global Times (via China Railway Kunming Group). (2025, March). Cargo transported via the China–Laos Railway.

His recent work examines the broader socioeconomic consequences of artificial intelligence, including labor markets, public finance, demographic change, institutional adaptation, and the distributional effects of technological progress.

He holds a PhD in Mathematical Finance from Boston University, and previously earned an MSc in Finance and Economics from the London School of Economics. He completed his undergraduate studies in Economics at Seoul National University under the Korea Foundation for Advanced Studies scholarship program.