[AI and Tax] Taxing AI Profits in Europe

Published

Keith Lee*

*Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

AI does not generate a distinct, separable tax base. Returns arising from AI, which may be reduced by deductions, tax credits and refundable tax credits, are typically combined with returns on software, proprietary data, organizational capital, intellectual property, market power and complementary investment. A narrowly defined AI tax is therefore administratively costly and likely to discourage productive adoption. This article examines how the European Union can capture economic rents and profits arising from AI without taxing its use. It distinguishes ordinary returns from economic rents, considering the various uses of Pillar One, Pillar Two, digital services taxes, capital-income taxation, cash flow and allowance-for-corporate-equity arrangements, excess-profit taxation, rebalancing of business labor taxes and public participation in publicly financed research and development. These instruments differ in how they identify, allocate and tax mobile AI-related returns between Europe and other jurisdictions. The contribution suggests here that Pillar Two's minimum-rate floor reduces the incentive to reposition mobile profits elsewhere; but cannot allocate residual profit to EU customer and user markets, that Pillar One can play a role here but is not yet operational and that turnover-based digital platforms taxes can only serve as an imperfect interim proxy. The best course of action seems to consist of a modular and layered set of actions: pursuit of enforceable minimum tax, further multilateral negotiations on market- sharing, strengthening of taxation on realized capital income, examining broader rent-sensitive corporate tax reforms and mitigating the excessive burden of taxing too much of workers' labor income. Realized rents and shifted profits should be taxed instead of the algorithm itself.

[AI and Tax] is an independent research series developed by Professor Keith Lee following his presentation at the conference Inequalities in Longevity, held at Fondazione Giorgio Cini in Venice on 3–4 July 2026, and a subsequent substantive discussion with Federico Fubini of Corriere della Sera concerning AI-driven productivity, labour income, and fiscal capacity.

Public-facing adaptation

A public-facing adaptation of this research, written by the author for a wider readership, is available from The Economy Review: “[AI and Tax] Taxing AI Profits in Europe: Follow the Rent, Not the Tool .”

1. Introduction - Why Even a One Percent Revenue Loss Matters

The most secure starting point is not a thought experiment about all possible mass technological unemployment but a simple example of fiscal mathematics. Eurostat reports that taxes and net social contributions in the EU amounted to €7.281 trillion in 2024.[1] Total EU general-government revenue was approximately €8.29 trillion, so a one percent decline would have reduced annual receipts by about €82.9 billion.[2] This is not a civilization-endangering number; quite the opposite, it is unquestionably a fiscally significant loss. What's more, it is not an abstracted European aggregate. Eurostat data show 2024 tax-to-GDP ratios in the article’s focus countries, namely France, Italy and Belgium. They each registered in 2024 an intake of over 42 percent of their gross domestic product.[3] In economies of such a mass, even minuscule erosions of all-encompassing tax bases turn into budgetary consequences rather than rounding errors. It is the compositional, rather than AI, erosion of tax bases that makes the issue relevant for AI policy. This compositional concern is based on the fact that, according to the European Commission's latest data on the composition of the tax mix, in 2024, the most important sources of taxes in the EU-27 were labor taxes and social contributions, 51.5 percent of the total, followed by consumption taxes at 26.8 percent and capital taxes at 21.6 percent.[4]

Europe’s heavy reliance on labor and payroll taxation creates fiscal exposure if the composition of part of the value added shifts gradually and unevenly to profits, capital income, royalties, high mark-ups in intangible-intensive sectors and returns to capital ownership and capital gains, income that is more concentrated and more internationally mobile than wages. This does not mean disaster, but just that possibly even moderate compositional shifts might have an influence of fundamental importance for the public finance outcomes, given that European taxation of labor is heavily weighted and that of mobile capital in an environment of much less generous institutional restrictions. There is an equally compelling reason to avoid a naive response, however. A recent firm-level investigation by the European Central Bank demonstrates that while AI technology adoption is expanding, deep integration is only prevalent among a small minority: more than 70 percent of firms surveyed in the euro area reported usage of AI technology in 2025 and only 7 percent reported intensive AI use.[5] Furthermore, intensive users tend to cluster within high-tech sectors, younger firms and knowledge-intensive sectors[6] and the benefits from AI derive in significant measure not only from initial adoption but from the integration of AI into core processes, the investment in complementary assets and equipment and organizational overhaul. From a broader perspective, the OECD arrives at a similar bottom line: AI exhibits the qualities of a general-purpose technology; however, its productivity effects are uncertain, varied and reliant upon supporting assets and market configurations.[7] The intensive AI research and development is concentrated among a handful of leading technology firms and the diffusion of this technology remains uneven across industries. These factors are pertinent to the design of tax policies because they call into question the underlying assumption that it will be easy to make AI profit fully transparent and create a smooth, uniform and administratively straightforward tax base.

That distinction is critical. It has been particularly hard in principle (not just in practice) to establish a distinction between profit generated by AI and profit generated more generally by software, proprietary data, brands, organizational capital, scale, high fixed-cost and low marginal cost businesses, regulation, or simply good managerial skills. The OECD's analysis of MNEs and intangible capital shows that the foreign affiliates of MNEs generate proportionately more income with intangible assets and that that income is more concentrated in ICT, finance, business services, telecommunications and other value chains that are highly intangible.[8] Much of what a public debate would loosely call AI profit is therefore better viewed as a menu of gains from intangible capital and the organisation of firms, of which AI is one input among several rather than the sole source; field evidence on generative AI points in the same direction: larger productivity gains often require a reorganisation of processes and task reallocation, which means these gains accrue with the tool, the firm and its investments in complementary factors, rather than strictly to the algorithm.[9] Once this is acknowledged, the road to a more sensible core tax question becomes clearer. It is no longer whether Europe should invent a narrow tax whenever a firm utilizes AI. Instead, the issue becomes whether its current and planned tax instruments can effectively target the tax bases that AI is likely to increase or redefine: standard corporate income, economic rents, residual income attributable to sources of value that may be separately taxed (high-value intangibles), income that has shifted offshore into low-tax jurisdictions, capital gains accruing to founders and investors and value created from customers or end users residing in countries without significant physical presence.

This is also why drawing a line between ordinary return and rent is crucial. If AI makes existing standard corporate activities more productive by bolstering mundane decision-making and administration with AI systems, the additional return from the resulting profit-generating enterprise should, in principle, be no different from returns that result from other types of successful digital-oriented investment. If, in contrast, AI extends market power, data advantages, first-mover scale, control over frontier models, or its sustained advantage in proprietary investment, then some portion of the resulting income may be economic rent, which is potentially a more appropriate object for targeted taxation. Hence, the resulting argument is cautious rather than alarmist. Europe should be cautious in rushing to implement a narrow tax merely because the tax label is AI: such a tax will often be poorly aligned with the underlying economics and will tend to penalize productive adoption of a general-purpose technology too much. But it does not follow that abandoning a narrow AI tax justifies complacency. What it would justify is a different approach. It would justify something that prioritized much stricter anti-shifting rules, more credible minimum taxes, market-jurisdiction allocation when appropriate, broader and more principled rent taxes, suitable capture of capital gains and distributions and a judicious repositioning of tax resources away from over-reliance on labor. The key principle would not be a blanket avoidance of algorithm-specific taxes, but a more careful decomposition of where rents are generated, whether a given jurisdiction has the best case to tax those rents and how to do so in a way that causes the least damage to productive activity and innovative commercialization.

2. Current Approach: What Europe’s Existing Tax Framework Can and Cannot Capture

Today’s European and international solutions build on a real flaw of orthodox international taxation: standard corporate-tax apportionment assumes significant taxing rights follow materially substantial physical presence and that profit can be apportioned by using legal entities, functions, assets and risks.[10] The digitalization of the economy undermined those priors some time ago, even before the current wave of AI adoption. Large multinational firms can generate enormous revenue from a market without having any factory, shop, or employee there, by locating ownership of code, intellectual property and group financing elsewhere. Those were precisely the concerns addressed by the European Commission's proposals in 2018. One was to define a corporate-tax nexus on the basis of a significant digital presence, in essence, a digital permanent establishment.[11] The other would levy an interim digital services tax over revenues derived from online advertising, intermediation and user data, aimed at groups earning above €750 million in worldwide revenue and at €50 million in taxable EU digital-services revenue.[12] Neither succeeded: they both failed in a way due to the absence of unanimity, as many Member States favored instead reaching a solution through the OECD. The conceptual notion that an emerging 2018 turn makes sense remains apparent. If a firm is able to derive value from the monetizing of consumers, users and demand in Europe, without a real physical presence, then market jurisdictions have a substantive argument to claim portions of the tax base. This claim is further reinforced if user participation, network effects and data feedback loops form part of the value creation process. And such claims are becoming increasingly relevant as services become more deliverable by digital means and, where applicable, automatable.

2.1 Pillar One and Market-Jurisdiction Allocation

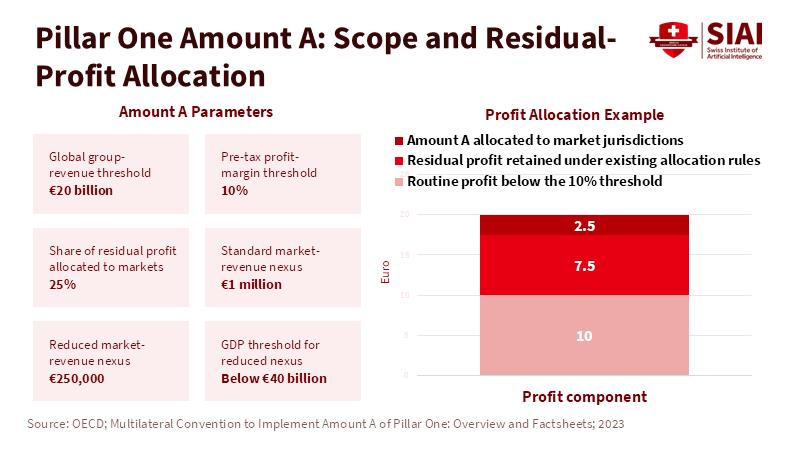

A recent analysis by the European Parliament looking at a potential EU digital levy finds that by 2023 digitally deliverable services accounted for 63 percent of EU cross-border services imports, while automated digital services accounted for 33 percent, rising to 39 percent when relevant IPR payments were included.[13] It also argues that AI is likely to broaden substantially the range of activities that can be produced digitally and supplied from the cloud.[14] AI therefore intensifies the existing cross-border provider-market problem. Nowhere is the problem of market-jurisdiction EU-wide corporate income tax and VAT/GST attribution and actual collection, in the context of cross-border provision, more profound. The OECD/G20 Inclusive Framework's Amount A under Pillar One was the solution to exactly that: a limited reallocation of residual profit to eligible market jurisdictions.[15] The OECD factsheets state that Amount A would be implemented just to the biggest, most-profitable multinational groups: those with adjusted revenues above €20 billion and pre-tax profit margin above 10 percent, with segmentation rules in a few cases where the Group overall is out of scope.[16] Of the profit exceeding that 10 percent level, 25percent of it would be apportioned to eligible market jurisdictions, as defined in the relevant paragraph of the OECD Implementation Framework text, according to sourced revenues.[17] The general market-revenue nexus would be €1 million, reduced to €250,000 for jurisdictions with GDP below €40 billion.[18] So the principle is not sectoral; it is a residual-profit-shifting redistribution to markets on broad economic indicator criteria.

Amount A is therefore attractive conceptually for Europe on at least three points: First, it allows the recognition that certain customer/user markets may be value creating without conventional physical presence; secondly, it attempts to tax residual profit rather than routine return and is therefore more conceptually aligned with rent allocation than to normal-source taxation; and thirdly, it provides a multilateral pathway for the phased elimination and standstill of digital services taxes and other similar measures, thus avoiding a proliferation of overlapping national instruments. The OECD factsheets also feature the Distribution and Marketing profits Safe Harbour expressly designed to mitigate double counting of profits where existing rules have already allocated significant profit to the market jurisdiction.[19] In principle, this renders Amount A preferable to unilateral turnover taxes, since it is profit- and threshold-based and established with the aim of avoiding double taxation, rather than layered on top of existing arrangements without the benefit of that integration. Practically, therefore, the main constraint is the current legal status of Pillar One. The OECD's current Amount A webpage indicates that the wording of the multilateral convention issued in October 2023 has not yet been opened for signature.[20] This webpage also confirms that the wording embodies the consensus so far reached, though certain issues remain unresolved; footnotes make these clear. The January 2025 co-chair update reported that the agreed text of the MLC had been submitted to the Inclusive Framework for adoption and clarified that adoption of the final text itself did not create any obligation to sign; the decision was to be made separately, according to domestic procedures.[21] The update explained that‚ since the adoption of the final MLC, discussions in the Inclusive Framework were focused on outstanding issues regarding the Amount B framework. Amount A is neither legally in force nor operational in 2026. By July 2026, therefore, Europe cannot treat Amount A as being implemented or effective.

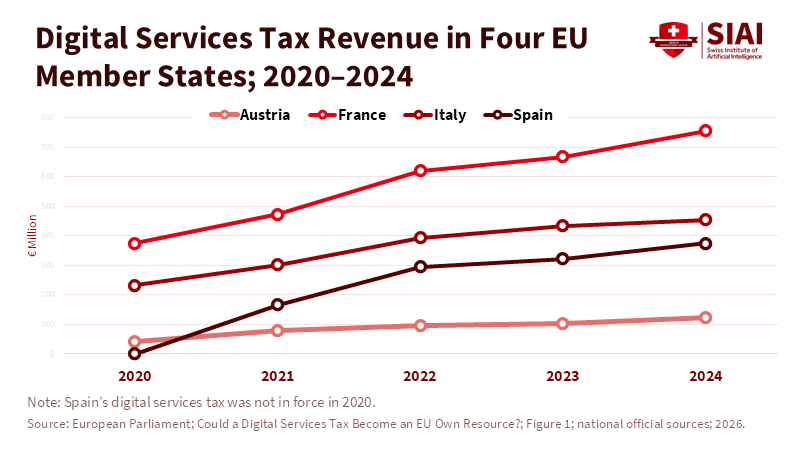

It is a negotiated but unrealized architecture. This remains an open issue and has kept digital services taxation and digital surcharges on the agenda within Europe. The EU's own resource based on a digital services tax was discussed in a 2026 briefing published by the EU Parliament, which stated that implementation of Pillar One had not materialized and that the absence of a global solution increases pressure for EU action. The briefing also confirms that France, Italy, Spain and Austria are already using domestic digital services taxes or similar levies and that these have generated predictable but limited revenues. In 2024, these states raised, for example, €756 million, €455 million, €375 million and €123 million, respectively. [22]

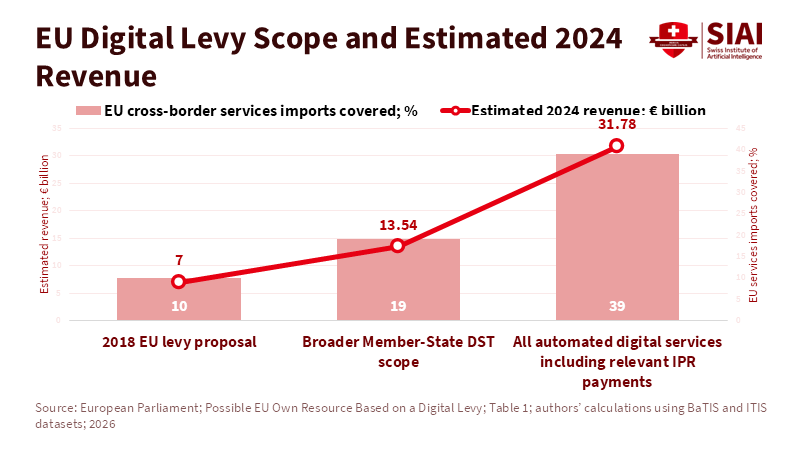

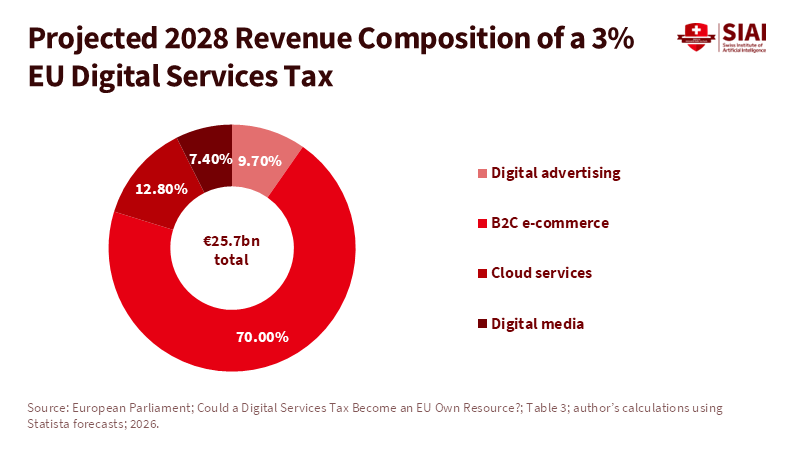

While this is not a fiscally transformative amount, it does tell us that gross-basis digital taxes are administratively plausible. At the same time, it encapsulates the key trade-off involved: a gross-basis DST will raise revenue relatively quickly, but it will do so through a fractured framework of thresholds and reporting duties that threaten to distort the rules of the Single Market. The wider digital-levy debate also illuminates the appeal and risks of unilateral action. The second European Parliament briefing on the 2026 digital-services-tax estimates that a DST limited to the narrow scope of the 2018 Commission proposals would cover about 10 percent of EU cross-border services imports and would yield about €7 billion every year. A broader scope, similar in coverage to the scope of DSTs already adopted in Member States, would cover about 19 percent of cross-border services imports and be expected to raise about €13 billion per year.[23] An even broader tax, covering automated digital services, including those enabled by AI and from the cloud, including those in cloud-based delivery models, would normally be expected to yield even higher revenue than the 6 percent of the presumably appropriate tax base estimated for the narrower spectrum of digital services that is possible to measure. Nonetheless, this material makes the administrative difficulties clear.

Once the base is broadened enough to approximate where AI-enabled value is really being captured, then what the measure most closely resembles is a broad tax on cross-border digital services, including intellectual property, not a tax on a narrow class of digital platforms. This may be more economically defensible than a purely AI levy, but it is also more politically and legally ambitious and closer to an import tax than the traditional concept of a rent tax.

2.2 Pillar Two and the Minimum-Tax Floor

Pillar Two addresses a different issue. The EU's Minimum Corporate Taxation Directive applies the OECD's 15 percent minimum tax for multinational enterprise groups and large-scale domestic groups generating more than €750 million in revenues.[24] The European Commission's current guidance page notes that when the effective rate in the jurisdiction is less than 15 percent, a top-up tax will apply through the Income Inclusion Rule, the Undertaxed Profits Rule, or a qualified domestic minimum top-up tax.[25] The European Commission also explains the policy motivation for the substance-based income exclusion it adopts: to ensure that a fixed level of income is ignored for tax purposes where there is a substantive level of payroll and tangible assets, thereby moving away from those excess profits that result from income shifting strategies and that tend to be rich in intangible assets that are at greater risk for tax planning.[26] As such, the Pillar Two plan is not a market jurisdiction allocation system. It is an anti-base-erosion floor and, at best, a simple anti-rent-avoidance proxy for highly mobile, low-taxed profit. The OECD's quantitative analysis provides a possible explanation for why Pillar Two is relevant even for the profit shifting associated with AI. It projects that the global minimum tax would cut global shifted profits in half, would cut the share of global multinational profits taxed below the 15 percent minimum tax rate by more than two-thirds and would generate an extra USD 155 billion-192 billion per year in global corporate income tax revenue.[27]

A report by the European Commission Joint Research Center looks at EU Member States and finds that in the short term, CIT revenue in the EU would increase by approximately 7.1 percent or around €26 billion per year) if all EU countries adopted the minimum-tax rules.[28] These are important, but the same studies also show the flaw. Pillar Two reduces the return from shifting mobile profit and intellectual-property income into low-tax countries. It does not, on its own, give market countries a higher share of residual profit just because there are customers or users there. So the two pillars are complements, not substitutes: one deals with the allocation; the other deals with the undertaxation and profit shifting. Thus, the argument presented here is that present arrangements are complex and incomplete and a clear indication that the present arrangements are only the beginning of the story: Europe has at present an effective Pillar Two framework. It has a powerful anti-shifting mechanism. Nevertheless, it lacks an effective, treaty-based system of residual profit allocation to markets and it does not possess an agreed-upon, workable common position on the utility of a purely temporary turnover tax in places where Pillar One remains frozen. While some cases can be made for the lack of market jurisdiction in a developing world and if the case is more weak elsewhere, the issues of primacy of source-based taxation, the difficulty of treaty revision and the associated technical complexities, the potential problems of overlap with unilateral measures and the continuing uncertainty surrounding the exact contents and legal effects of the multilateral convention argue that the present arrangements are, at least, incomplete: they impose taxes on some mobile AI-related profits to a greater extent than previously, but are uncertain as to where they will share further those profits amid inherently high user-based source-determined activity.

3. Alternative Taxation: Taxing AI-Related Profits and Rents Without Taxing AI Use

A robust examination of alternatives must first exclude at least one tempting but unfounded idea: an AI-specific tax base. There is no commonly adopted accounting or legal measure that can, for tax purposes, distinguish AI's contribution to profit from that of software engineering, specialist data, cloud infrastructure, brand capital, distribution channels, organizational design choices, or the strategic advantages that accrue as a result of other investments in scale. The OECD explains how the economic impacts of AI very much depend on pervasive complementary innovation, diffusion and market structure.[29] Existing research at the firm-level seems to agree: strong value is only realized if AI is embedded in a business through large-scale projects and restructuring. For multinationals, returns on intangible capital are also already inextricably spread across affiliated firms, different tax jurisdictions and various asset categories. The most plausible taxable consequences of the AI transformation, then, are not a profit account for AI in particular, but such things as increased gross margins, royalty streams, high residual profit shares, founder exits, dividend payouts and share prices that anticipate future rents.

3.1 Pillar Two as a Minimum-Tax Floor

The first and strongest alternative instrument, therefore, is not a new AI tax but a more effective implementation of Pillar Two. That has two advantages; it rests on a tax base that exists in law and it directly confronts one of the main weaknesses of AI-intensive business models: the ability to position highly mobile, lucrative intangible incomes in low-taxation jurisdictions. The EU has moved ahead of many peers by transposing the minimum-tax directive for fiscal years beginning in 2024. Just as the 2026 Commission-supported manual for 14 participating Member States demonstrates, considerable variations therefore persist within a shared legislative framework in registration, filing and payment rules, designated entities and centralized compliance.[30] Better implementation, therefore, not only entails simply sustaining the directive but also improving administrative coordination, information sharing, safe-harbor certainty and domestic capacity so that the floor bites effectively on mobile intangible profits.

Making an argument for such a strengthening is both conceptual and empirical. OECD estimates mean that the global minimum tax substantially reduces profit shifting benefits; the Commission's JRC study found that even taking account of long-term behavioral impacts, the direct tax effects for the EU were sizeable. This is especially relevant where AI-related rents are not such as to flow through to findings of rent in property rental markets, for example, but where these rents are captured in intellectual-property income, other forms of mobile, hard-to-value profit. Furthermore, Pillar Two’s structure already reflects a normative judgment of a sort that is key to this paper's core distinction: the substance-based exemption ensures coverage of a formulaic return linked to tangible assets and payroll, while more residual, intangible-intensive rents are left exposed to the top-up tax. It is far from a perfect approach to distinguish mobile residual income from normal returns and unintended consequences can be avoided simply by moving in that direction. But Pillar Two cannot shoulder the entire policy burden. It does not instruct Europe on which jurisdiction imposes tax on global profit generated by final consumption or user markets, or what have you. It restricts the advantage of declaring profit in a low-tax jurisdiction. Finally, it is not beyond the scope of avoidance via credit-mix, subsidy, classification choice, or under-enforcement induced by internal complexity. To conclude, it is the best tool for AI as a protection of the floor. It can sort out part of the globally mobile profit that drifts without tax; it cannot allocate the resulting tax to the Irish, French, German, Italian, or non-European parent jurisdiction that obtains the revenue from the customer-generating activity.

3.2 Economic-Rent and Excess-Profit Taxation

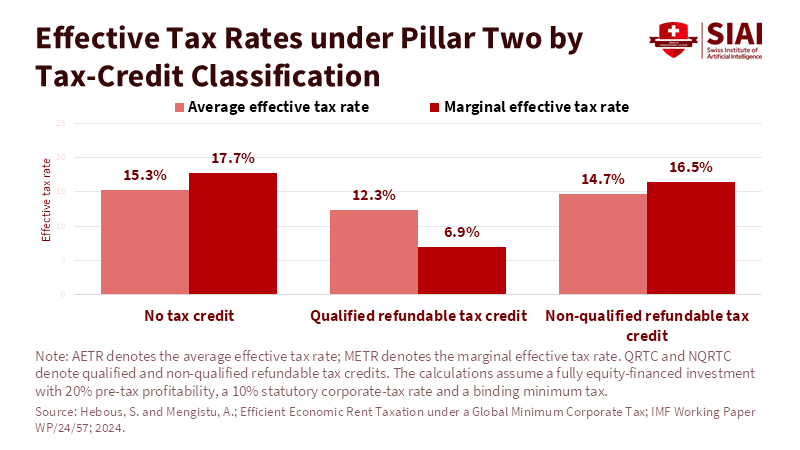

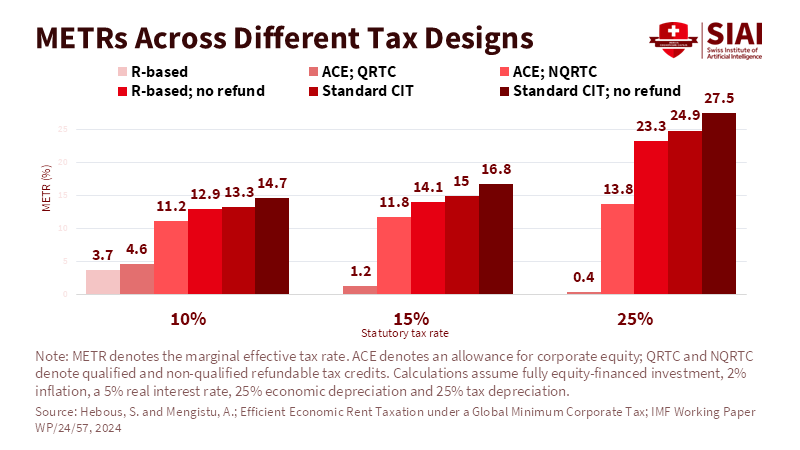

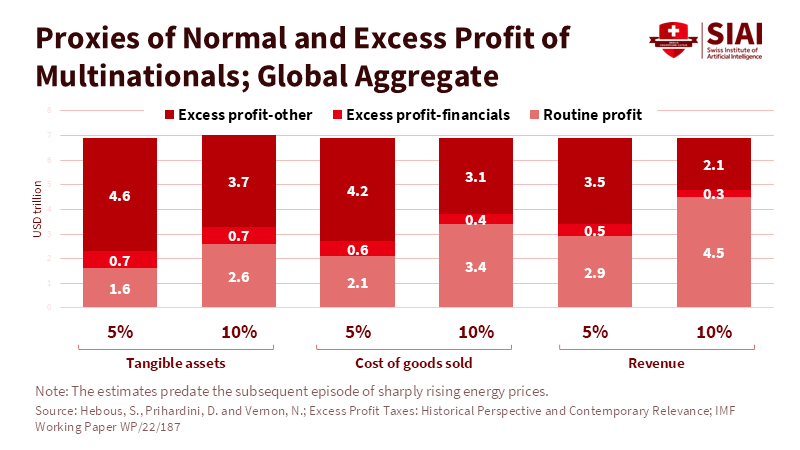

The second, more serious, family of alternatives is economic rent or excess-profit taxation. The case is supported by the work of Hebous and Mengistu, who define economic rent as returns in excess of opportunity costs and argue that well-designed rent taxes need not be distortionary, thus providing an efficiency argument for rent taxation: the inverse of what we have seen so far.[31] The IMF identifies two broad operational models for excess profit taxes; one is cash-flow taxation, which effectively affords up-front expensing of investment, thus exempting the normal returns from economic rents while taxing away the above-normal return.[32] Second, it is a system that envisages an allowance for the normal return through an allowance for corporate equity.[33] This resembles advanced conventional accounting practices: a notional deduction consistent with what interest payments on debt provide. Instructively, Hebous, Prihardini and Vernon reach a similar conclusion and show that, at least theoretically, excess-profit taxes can be targeted exclusively on those rents thus understood, with the resultant policy remaining non-distortionary. In theory, then, taxing rents and not AI-enabled profit is the superior, elegant countermeasure to the risk of discouraging marginal investment. The problem is that this neat conceptual scheme of rent taxation collides with the administrative disarray of AI production. To even know what an AI rent might be is extremely difficult. Value created by AI is often imprecise, wrapped up with off-the-shelf software, embedded in consulting contracts, subsidized through platform ecosystems, shielded by patent structures, or achieved only as a means to inflated equity prices.

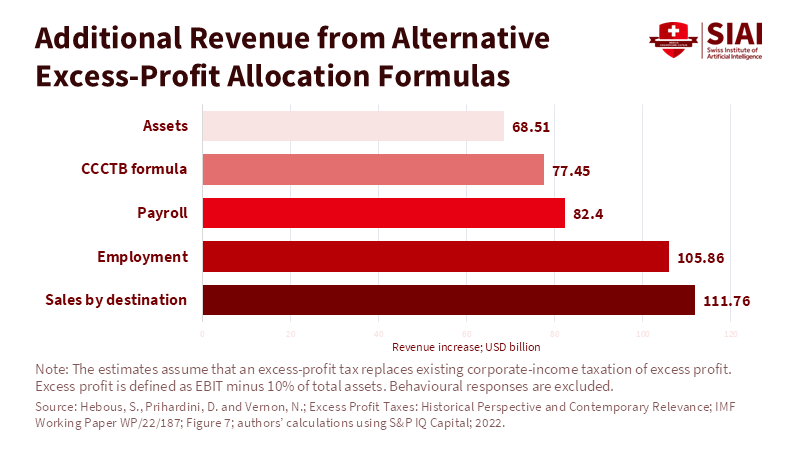

Even separating a normal return from rent within a single firm proves challenging; calculating a firm’s normal cost of capital, accounting for losses and carry-forwards, valuing intangibles under fair-value accounting and establishing an objectively credible method to apportion a corporate group's rent across many different countries all are administratively difficult. In various cross-border contexts, all those difficulties are compounded by group structures and transfer pricing, the strategic place of ownership over the highest-value intangibles. Now that AI tends to foster scale increases and intangible intensification, perhaps the rent values it is easiest to grab will be the most finely-grained and hardest-to-measure. These constraints lead to two conclusions. First, if Europe intends to move towards a system of rent taxation at all, it will need to do so by implementing broad reforms to its corporate tax base rather than by measures targeting an AI rent tax in particular. Extending a safe harbour for normal returns, or proceeding to ad hoc cash-flow reforms would at best generate a tax on AI rents where they exist, but would also capture rents from other activity associated with high levels of intangible investment or distinctiveness, which would arguably be a benefit if the standard engendered by the normative goal in the first place is to attribute tax to rents regardless of the technology that underpins them.

Second, any rent-based tool will still depend on a territorial rule where capital markets operate. A rent tax limited to the territorial sphere of legal taxable events of a corporate entity, or in which an intangible is constituted or is a former company property, will not prevent the market complementarity problem. A rent tax based on destination or formula will provide greater stability against shifting, but will require the implementation of a system akin to formulary apportionment or destination-based cash-flow tax, rather than incremental reform. For Europe, this may be a long-run evolution rather than an immediately deployable tool. A supplemental excess-profit tax is a compromise, somewhere between the ideal and the practical. As the IMF review notes, excess-profit taxes have often been introduced in wartime and during other episodes of acute windfall gains and in such circumstances, a time-limited levy on large profits remains defensible even when baseline calculation is necessarily incomplete.[34] But that analogy does not transfer well to AI. It is not a once-and-for-all energy-supply shock and the AI industry is not an established tax domain. An ongoing, across-the-economy excess-profit charge designed specifically for AI would be hard to justify. A short-term, wide-angle supplemental excess-profit levy might still make sense if Europe encountered a situation of readily identifiable and concentrated rents in a few fiercely supported or exceptionally protected sectors. But this is a final-resort mechanism, not the core framework to regulate AI rents.

3.3 Capital-Income and Digital-Services Taxation as Complementary Instruments

Capital gains and dividend taxation are less directly targeted than an effective rent tax, but for some areas, they are closer to the point at which AI-related gains are realized. Much of the economic upside of successful AI deployment will not end up as continuously taxable profit in Europe: instead, it may be capitalized into share values, founders’ wealth, venture-stage exits, acquisitions of start-ups, or distributed to shareholders in high-income households. OECD work on capital gains has found that most OECD countries tax capital gains on realization, frequently at lower rates or with exemptions in comparison to other income, partly on grounds of dynamism, though there is inconclusive evidence that these implementations significantly influence growth.[35] For Europe, then, this suggests a pragmatic complement rather than a successor. Broad-based and reasonably integrated taxation of capital gains and dividends may allow a share of large potential windfalls of AI to be captured without directly taxing companies that use such AI. However, whether as a consequence of unrealized gains remaining unrealized, individuals or firms leaving, large gross gains being unrealized for a long period of time, or corporations seriously considering exit-tax regimes, it is obvious that this is a less than perfect measure, with obvious mobility and innovation-related drawbacks for founders, entrepreneurs and high-net-worth, high-mobility households. A reasoned plan for capital-income taxation should therefore follow an eminently cautious approach. Europe has legitimate reasons to be cautious about reducing unwarranted differences between taxing labor income and taxing realized capital gains or dividends, particularly where entrepreneurial risk increasingly clearly manifests itself as returns to scalable intangibles. It also has reason to defend doing so by claiming a significant tax benefit where the countries could raise an AI-specific capital-gains tax by precluding any leakage into exit jurisdictions. Yet assigning all AI-related capital gains to a separate tax would reintroduce the main flaw of a narrow AI profit tax. It would blend innovation rents and regular entrepreneurship risk and encourage residence-based tax planning.

Europe would better aim at improving general capital-income taxation and its mitigation than at applying an AI label to it. Turnover taxes and digital levies remain the most tempting unilateral option because they combat one genuine problem head-on: value created and realized in European markets without a tangible taxable footprint. The 2026 European Parliament briefings demonstrate why they remain a politically credible option. Revenues are highly visible; administration is comparatively straightforward and profit-shifting matters less because the dominant base is turnover. Country experience also indicates that revenues have been more resilient than many detractors initially contended. The same 2026 briefings also show why they are a poor long-term basis for taxing AI-related profits. They fail to differentiate between profit streams and rents. They risk taxing low-margin, high-growth firms at the same rate as high-margin market incumbents. They may shift costs onto merchants, online advertisers and end-consumers. They threaten Single Market integration if transposed to their likely multiplicity of national configurations. A more comprehensive levy on automated digital services might be slightly more rational than a narrow Digital Services Tax, but it remains intrinsically a gross-basis tax that by design can only roughly estimate rent capture. That said, the appropriate treatment of DSTs is therefore a matter of prudence. They are not suitable tools for establishing or taxing AI profit. However, they are plausible interim measures to tax market-based value in the absence of treaty-based residual-profit sharing, should national governments be unwilling to wait indefinitely for the aforesaid Pillar One arrangement.[36] If adopted at the EU level, the most approachable form ought to be EU-wide rather than national, specifically temporary as opposed to perpetual, designed to replace rather than accumulate on top of regional DSTs, in addition to a sunset or modification clause in case a worldwide market-sharing framework eventually functions. But even then, it should be promoted as a digital turnover substitute for market access, rather than a levy on AI itself.

3.4 Labor-Tax Rebalancing and Public Participation

Another set of considerations pertains to the overall fiscal composition. The Commission's own figures demonstrate that Europe remains atypically dependent on the collection of taxes on labor. Such dependence has a particular policy risk: that if AI increases productivity but dampens the growth of the labor-tax base, governments may attempt to offset the effect via increased charges akin to the labor-related burden on firms at the technological frontier that are subject to AI or on labor-saving technologies themselves. This would be unwise. The Commission's own work on taxes repeatedly contends that reallocating more of the burden away from labor and onto environmental taxes and recurrent immovable-property levies can be done fairly and efficiently and its 2024 Annual Report on Taxation found that perhaps, to forestall falling revenues, Europe may need to transition away from labor towards capital and consumption taxes in the medium term.[37] The key point for the present discussion is thus a cautionary one: Europe should not follow the rest of the world in subjecting itself to a quasi-robot tax that increases the marginal cost of adopting AI. A much less ambitious rebalancing would be more modest and more defensible. It would maintain incentives for an efficient use of AI by mitigating, at the margin particularly where labor-tax wedges are high, the tax penalty on formal employment and routine labor at the margin and only partially fund this mitigation by broadening, in a way less sensitive to adoption, less mobile domestic tax bases, including recurrent property taxes, environmental taxes, enlarged and realised capital-income collection, improved policing of base erosion.

It would remove the built-in, or at least embedded, labor tax cost to AI and, more generally, to more successful intangible deployment, without giving up on the gains characterized by consumer surplus and quality improvements, which, because they do not constitute realized taxable income, should be left untaxed. Finally, there should be modest but serious consideration of public participation in the upside. Where public funds materially reduce the risks involved in follow-on commercialization, ex post taxation is not the only means of securing fiscal capture. The European Innovation Council already stands as an institutional precedent, if one that remains to be refined; its EIC Fund functions as a venture-capital arm, capitalized at more than €4 billion, while EIC Accelerator funding can be combined with substantial equity investment.[38] A financial stake in this narrower area than general taxation should involve the granting of warrants, royalty-like repayment clauses, convertible instruments, or minority equity holdings, so that direct taxpayers benefit from commercial success rather than socializing losses. This principle is most tenable in cases where support is concentrated, additive, risky and targeted at the development of critical and autonomous AI-related capacities; least tenable where it is applied on an indiscriminate basis, crowds out private resources, or is distorted by political selection. Public upside participation can be an adjunct to taxation; it cannot be an alternative to a rationally designed tax system.

Taken together, these considerations argue for a layered European policy approach. The first layer should be the full, credible administration of Pillar Two, which is the particular solution to the fact that anti-shifting is a pressing and otherwise solvable problem. The second layer should be the persistent effort at a multilateral market-allocation mechanism under Pillar One, without any pretense that its data, much less tax rules, are operational. The third might be the search for broader rent-tax principles, perhaps allowances for normal returns, cash flow, or carefully delimited excess-profit components without AI as a supposed separate object of tax. The fourth should be the targeted bolstering of capital-gains, dividend and exit tax regimes where households are actually experiencing the AI rents. The fifth should be a redefinition of the tax mix, balancing dependence on labor with income from capital and wealth. Once those five layers are in place, the eye-catching idea of a temporally coordinated but geographically limited and administratively manageable EU-wide DST, as something that might initially pick up some of the slack of a below-cost AI tax, might be permissible, if not entirely inevitable. What is obvious is that tax bases affected by AI should be approached through the instrument best matched to that particular phenomenon (profit-shifting, market access, rent, realized wealth, or excessive dependence on labor), rather than through the rhetorically appealing but administratively fragile AI-specific tax.

Conclusion - Tax the Rent, Not the Algorithm

Europe should avoid a narrowly defined tax triggered solely by the use of AI. It is impossible to distinguish AI-related gains from other gains in software, data, brands, organizational capital and complementary investment, nor can it distinguish the label “AI profit” from normal returns or economic rents. The more defensible policy principle is thus to tax the rent, not the algorithm, while treating identifiable local infrastructure and environmental costs separately from internationally mobile profits. No single instrument provides a complete solution. Pillar Two can limit the benefit of locating low-taxed profits in favorable jurisdictions, but it cannot allocate residual profit to European customer or user markets. Pillar One is designed to do so and Amount A is not yet operational. Broader reforms based on the principle of cash-flow taxation or allowances for normal returns are attractive in principle but difficult to administer globally. Capital gains and dividend taxation can capture some realized gains, while a temporary EU-wide digital-services tax may provide a short-term market-based proxy, but turnover taxation can disadvantage low-margin firms and be passed through to consumers. Thus, the most credible European policy requires a layered reform package: enforce the minimum-tax floor, continue multilateral market-allocation negotiations, strengthen taxation of realized capital income, examine broader rent-sensitive corporate-tax reforms and reduce excessive reliance on labor taxation without discouraging productive AI adoption.

This article was prepared as an independent research contribution following Professor Keith Lee’s presentation at the conference Inequalities in Longevity, held at Fondazione Giorgio Cini in Venice on 3–4 July 2026, and a subsequent substantive discussion with Federico Fubini of Corriere della Sera. The discussion helped sharpen the motivating questions concerning AI-driven productivity, the declining employment intensity of economic growth, and the resulting pressures on the public tax base.

The research, analysis, and conclusions were developed independently by the author. This publication is separate from the official conference proceedings and from the editorial coverage published by Corriere della Sera.

Unless expressly stated otherwise, this publication has not been commissioned, reviewed, or endorsed by Fondazione Giorgio Cini or Corriere della Sera. References to the conference and the subsequent discussion describe the intellectual context in which the research developed and do not imply co-authorship, institutional affiliation, formal collaboration, or partnership. The analysis, interpretations, and conclusions are those of the author and do not necessarily reflect the official positions of Fondazione Giorgio Cini, Corriere della Sera, the Swiss Institute of Artificial Intelligence (SIAI), or their respective affiliates.

References

[1, 3] Eurostat (2025) EU and euro area tax-to-GDP ratio up in 2024. Luxembourg: Eurostat.

[2] Eurostat (2025) Euro area government deficit at 3.1% and EU at 3.2% of GDP. Luxembourg: Eurostat.

[4] European Commission (2026) Data on Taxation Trends. Brussels: Directorate-General for Taxation and Customs Union.

[5] European Central Bank (2026) Survey on the Access to Finance of Enterprises in the euro area: Fourth quarter of 2025. Frankfurt am Main: European Central Bank.

[6] Chaloupka, D., Lalinský, T. and Lopez-Garcia, P. (2026) What separates firms that use AI intensively from firms that don’t? Frankfurt am Main: European Central Bank.

[7, 29] Filippucci, F., Gal, P., Jona-Lasinio, C., Leandro, A. and Nicoletti, G. (2024) ‘The impact of artificial intelligence on productivity, distribution and growth: Key mechanisms, initial evidence and policy challenges’, OECD Artificial Intelligence Papers, No. 15. Paris: OECD Publishing.

[8] Cadestin, C., Jaax, A., Miroudot, S. and Zürcher, C. (2021) ‘Multinational enterprises and intangible capital’, OECD Science, Technology and Industry Policy Papers, No. 118. Paris: OECD Publishing.

[9] Calvino, F. and Fontanelli, L. (2023) ‘A portrait of AI adopters across countries: Firm characteristics, assets’ complementarities and productivity’, OECD Science, Technology and Industry Working Papers, No. 2023/02. Paris: OECD Publishing.

[10] OECD (2022) OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2022. Paris: OECD Publishing.

[11] European Commission (2018) Proposal for a Council Directive laying down rules relating to the corporate taxation of a significant digital presence, COM(2018) 147 final. Brussels: European Commission.

[12] European Commission (2018) Proposal for a Council Directive on the common system of a digital services tax on revenues resulting from the provision of certain digital services, COM(2018) 148 final. Brussels: European Commission.

[13, 14, 23] Amaro, F. and Picciotto, S. (2026) Possible EU own resource based on a digital levy: Cross-border services trade, digital transformation and tax implications. Brussels: European Parliament.

[15] OECD (2026) Reallocation of Taxing Rights to Market Jurisdictions. Paris: OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

[16, 18, 19] OECD (2023) Multilateral Convention to Implement Amount A of Pillar One: Overview and Factsheets. Paris: OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

[17] OECD (2023) Explanatory Statement to the Multilateral Convention to Implement Amount A of Pillar One. Paris: OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

[20] OECD (2026) Multilateral Convention to Implement Amount A of Pillar One. Paris: OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

[21] OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (2025) Pillar One Update from the Co-Chairs of the Inclusive Framework on BEPS. Paris: OECD.

[22, 36] Thomadakis, A. (2026) Could a digital services tax become an EU own resource? Revenue potential, policy trade-offs and strategic options. Brussels: European Parliament.

[24] Council of the European Union (2022) ‘Council Directive (EU) 2022/2523 of 14 December 2022 on ensuring a global minimum level of taxation for multinational enterprise groups and large-scale domestic groups in the Union’, Official Journal of the European Union, L 328, pp. 1–58.

[25] European Commission (2026) Minimum Corporate Taxation. Brussels: Directorate-General for Taxation and Customs Union.

[26] OECD (2021) Tax Challenges Arising from the Digitalisation of the Economy: Global Anti-Base Erosion Model Rules under Pillar Two. Paris: OECD Publishing.

[27] Hugger, F., González Cabral, A.C., Bucci, M., Gesualdo, M. and O’Reilly, P. (2024) ‘The Global Minimum Tax and the taxation of MNE profit’, OECD Taxation Working Papers, No. 68. Paris: OECD Publishing.

[28] Brun, L., Pycroft, J., Speitmann, R., Stasio, A.L. and Stoehlker, D. (2025) The impact of the global minimum tax on corporate tax revenues: Evidence for EU Member States. Seville: European Commission Joint Research Centre.

[30] European Commission (2026) Manual for MNE Groups on Global Minimum Tax (Pillar Two) Compliance Obligations. Brussels: Reform and Investment Task Force.

[31, 32, 33] Hebous, S. and Mengistu, A. (2024) Efficient Economic Rent Taxation under a Global Minimum Corporate Tax. IMF Working Paper WP/24/57. Washington, DC: International Monetary Fund.

[34] Hebous, S., Prihardini, D. and Vernon, N. (2022) Excess Profit Taxes: Historical Perspective and Contemporary Relevance. IMF Working Paper WP/22/187. Washington, DC: International Monetary Fund.

[35] Hourani, D. and Perret, S. (2025) ‘Taxing capital gains: Country experiences and challenges’, OECD Taxation Working Papers, No. 72. Paris: OECD Publishing.

[37] European Commission (2024) Annual Report on Taxation 2024: Review of Taxation Policies in the European Union. Luxembourg: Publications Office of the European Union.

[38] European Innovation Council (2026) European Innovation Council 2026 Work Programme. Brussels: European Commission.