[AI and Tax] Labor Income, AI Rents and Fiscal Erosion

Published

Keith Lee*

*Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

Artificial intelligence does not mechanically erode the tax base; the fiscal impact depends upon how the productivity gains are shared and where the income generated is taxed. This paper studies AI as a productivity shock, an income-distribution shock and a fiscal-transmission shock. It separates task automation from job displacement, firm productivity from macro employment effects and ordinary business returns from AI rents. The evidence suggests that generative AI can create productivity gains in selected tasks, particularly for lower-skilled workers,but has not yet produced broad employment displacement. Nevertheless, it is uncertain whether output resulting from such gains will always offset labor substitution in sectors with weak demand growth, in concentrated markets or where complementary investments are lacking. Accordingly, the fiscal impact will rest on whether such gains are ultimately paid to workers, consumers, domestic firms, investors, or foreign AI suppliers. Countries that rely heavily on labor taxes and social contributions, import substantial AI services or tax capital income weakly may be most affected. The most pressing policy dilemma is not in taxing AI as a technology, but in safeguarding the domestic tax base as digitalization shifts income from broad, immediately taxed payroll remuneration to more concentrated, mobile, or deferred forms of income.

[AI and Tax] is an independent research series developed by Professor Keith Lee following his presentation at the conference Inequalities in Longevity, held at Fondazione Giorgio Cini in Venice on 3–4 July 2026, and a subsequent substantive discussion with Federico Fubini of Corriere della Sera concerning AI-driven productivity, labour income, and fiscal capacity.

Public-facing adaptation

A public-facing adaptation of this research, written by the author for a wider readership, is available from The Economy Review: “[AI and Tax] Why AI Fiscal Erosion Begins Before Jobs Disappear”

1. Introduction - Does AI Replace Tasks or Complement Workers?

AI can achieve superhuman performance on selected tasks, but it cannot create a superhuman worker. For example, modern classification, summarising, translating, editing, compiling, searching, document comparison, pattern recognition and generation technologies can perform certain activities at a speed that is significantly faster than unassisted humans. Many processes that took days may now take hours. But the largest demonstrations of task acceleration can hardly be taken as evidence that the overall productivity of a professional, such as a lawyer, has been multiplied ten times. The agent’s job may again involve problem framing, fact checking, forecasting, communication, coordination and responsibility for error. AI may accelerate one step of an otherwise unchanged procedure or a new requirement for review or oversight may be introduced.

The strongest experimental and workplace evidence points to material but bounded productivity improvements. In a randomized trial of professional writing tasks, providing generative AI access cut average task duration by 40 percent and boosted average assessed quality by 18 percent.[1] A study of customer-support agents shows that an AI assistant resulted in about 14 percent more issues resolved per hour on average, with substantially larger improvements among relatively inexperienced and initially lower-performing workers.[2] In a randomized trial of management consultants, AI usage led to more task completions, hastened completion speed and better answers when assignments hovered within the model's capability frontier, but to poorer answers on some tasks designed to be at least partly outside of that frontier.[3] The empirical case thus tilts towards selective amplification rather than a universal productivity multiple across intellectual work.

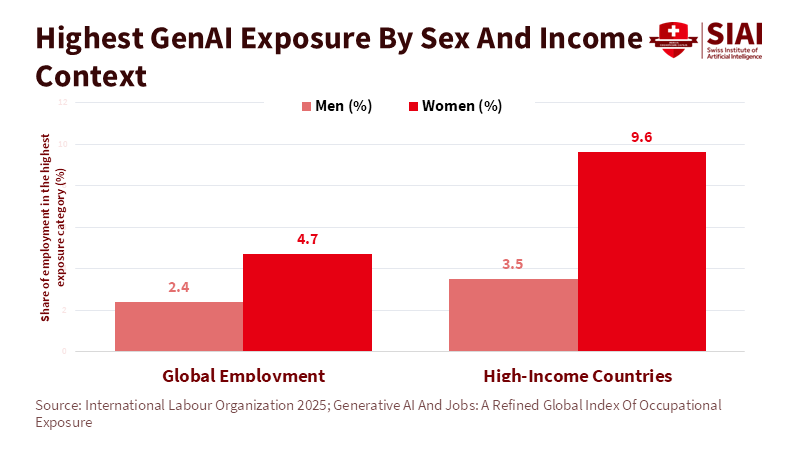

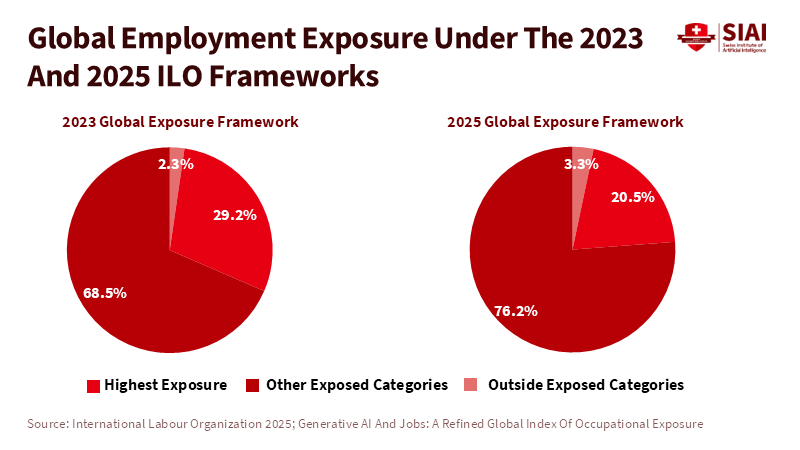

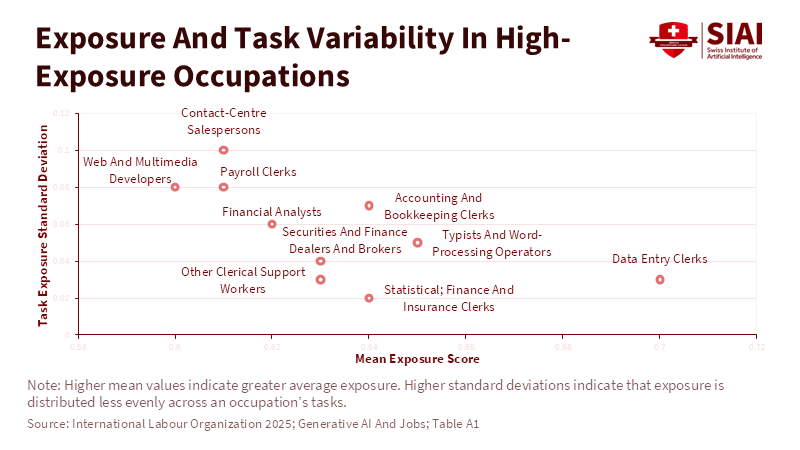

This distinction is important because the work task is often conflated with the entire job. A model could generate a draft version that automates but does not displace the task of a worker who defines the goal, checks the output and assumes professional responsibility. A worker can complete a routine job analysis faster but needs more time to do unusual analyses or advise customers. A company can output less labor content to accomplish one internal procedure, while increasing sales, quality, or new services. An economy can eliminate some tasks and still create new jobs in implementation, verification, data stewardship and customer service.The International Labor Organization's refined global index of occupational exposure underscores this gap between predicted exposure and employment displacement. It estimates that approximately 25 percent of global jobs are exposed to some degree of generative AI, with only 3.3 percent experiencing the highest levels of exposure.[4] Exposure level is highest in high-income economies (34 percent) but still low in the lowest-income countries at 11 percent[5] due to the preponderance of clerical, professional and digitized service work in the global North. Clerical jobs are the most exposed, but the International Labor Organization finds this unlikely to lead to complete job replacement, as most occupations blend activities subject to augmentation or automation with other activities requiring human input nonetheless. Measures of exposure are thus indicators of the technical feasibility of automation should it be adopted, not the probability of unemployment, nor a timeline for displacement.[6]

Macroeconomic estimates are closer to the more moderate of the task-level results. Acemoglu's task-based study, for which he approximates the effects of presently available AI applications, reports them as being potentially substantial but, in aggregate terms, modest over ten years, with total-factor-productivity improvements below the more revolutionary estimates typically ascribed to generative AI.[7] Early labor-market evidence has also failed to justify a prediction of employment losses across the economy. Administrative evidence from Denmark, tracking exposed occupations and thousands of workplaces, found no statistically significant net effect on earnings or recorded hours in the first two years of widespread chatbot adoption.[8] That survey nonetheless documents several new tasks associated with implementation, oversight, integration, ethics and compliance. An alternative analysis of occupational task exposure indicates that increased mean AI exposure in affected occupations can decrease labor demand in the occupations themselves, whereas only mixing AI concentrations over a subset of a job’s tasks allows workers to reallocate effort, while enough productivity growth at adopting firms to counteract its direct substitution is somewhat, yet not fully, offset by scale effects, yielding much more modest total employment changes than one would expect based solely on simulated task exposure effects.[9]

AI should therefore be interpreted as comprising three shocks at once. It is a productivity shock, in the sense that it may lessen the human effort and time necessary to undertake some particular types of activity. It is an income-distribution shock, in that the generated surplus will flow to one or another of labor, consumers, adopting firms, technology suppliers, investors, or scarce complementary employees. It is a fiscal-transmission shock, in so far as such recipients will be taxed through various mechanisms, at various effective rates, at different times and in different jurisdictions. Personal income tax, social contributions and payroll taxes are collected relatively quickly, whereas retained profits and unrealized capital gains may find their way into the domestic fiscal system more distantly. Hence, the central case should be put to the test and not taken for granted. The increased fiscal erosion will be more likely if substitution effects outweigh augmentation and scale expansion, if output increases are too small, if wage pass-through is weak, if rents are highly concentrated and if a large share of the technology payment or the proceeds of technology ownership arise outside the country that is home to the workers and customers. Gross domestic product is not equivalent to domestic fiscal capture.

2. Do Firms Expand Output Enough to Offset Labour Displacement?

Given a level of output, successful automation will require less labor for a given output. This accounting relation is commonly cited as a prediction of job destruction, though it describes only the initial phase of adjustment. Cheaper unit costs can be used to lower prices, increase quality and delivery speed, raise margins, or free up resources for new products and if demand grows enough, a firm may still be able to produce more goods with the same number of jobs, or raise employment while still reducing the labor hours needed per unit. The ability of expanded scale to offset displacements will depend on the elasticity of demand, competition, availability of capital and organizational capacity and on how much of the production process AI is capable of improving.

The relevant level of analysis is the task. An automated task can be defined as a task for which an AI-enabled workflow can produce a sufficiently acceptable output with little or no additional human input. An advantaged task involves the use of AI in a way that extends the speed, scope, or quality of work performed by a worker. An affected task is one in which there is some amount of partial automation, but which produces additional work in areas such as verification, communication, documentation, or other transaction costs. Jobs are constituted with some mixture of such task categories.[10] Firms use compositions of job task bundles that vary substantially. An accounting clerk sending data to or from a standardized system, such as VAT returns, might be reduced to ordinary substitution; by contrast, an accountant using the system to analyze complex transactions might receive means of augmentation.

Firm-level European evidence supports the possibility of expansion. Akin to a finding reported in the European Investment Bank’s 2026 assessment of about 13,000 firms in the European Union and the United States, where AI adoption in European firms is associated with stronger productivity performance without establishing a uniform employment effect[11] and the strongest benefits seem to accrue to medium-sized and large firms that can combine AI with investments in software, information and skills and organizational capacity.[12] While not being able to establish that all adopting firms expand and that all occupations are protected in all adopting firms, these results can hardly be interpreted as contradicting the idea that the direct labor effect of AI can be offset at the level of the firm when the investments in complementary factor inputs and the output growth are sufficiently large.

A firm may grow, even if industry employment falls. It can happen if more productive early adopters take market share from other poor performers, raising their employment but reducing sectoral labor demand; or if the cost savings give rise to firm-specific new demand by boosting output, thus raising employment in the whole sector. Hampole et al. assist in distinguishing these processes. Their task-based proxies indicate that occupations in which the average exposure to AI/machine-learning abilities is higher suffer lower relative labor demand.[13] However, this effect is mitigated when only some of an occupation's task package is exposed, as workers can compensate by intensifying other, less exposed activities. At the firm level, demand for labor related to increased productivity tends to compensate for much of the reduction in demand caused by the exposure of existing tasks.[14] The overall impact thus remains relatively weak vis-à-vis the occupational substitution effect. This does not imply that all former employees will be retained, since expansion might draw more workers into other occupations, plants, or skills. It demonstrates that automation in tasks does not equate with total employment.

The scale response is sector-specific. In software, consulting, marketing and some professional services, lower production costs can enable doing more projects because the incremental cost of serving one more customer is low and there might be a significant latent demand. In the private and public healthcare, education and administration sectors, it won’t necessarily generate commercial sales but will accelerate throughput or improve quality. The fiscal benefit may appear by decreasing waiting time or allowing the same staff to serve more users. On the other hand, relatively fixed demand seems to apply to long-established back-office functions. Consequently, double the number of reconciliations, reports, or activities would not be realized just because AI enables them to be cheaper and faster. How the increased saving translates into expansion depends on the level of contestability. The firm, in a competitive market, is willing to cut prices or increase quality to the extent that it keeps its market share, which would increase demand and share some of this gain with consumers. If the market power is high, the savings are reflected in a bigger margin, thus curbing the scale effect. Thus, employment effects may be stronger in contestable markets and weaker in concentrated ones.

The market structure influences the share of static surplus, which goes to the innovator, customers, or the upstream technology supplier. The pattern of adjustment makes interpretation less straightforward. In the short run, firms frequently implement AI within current procedures. Employment contracts, uncertainty regarding precision, legal standards and organizational inertia constrain direct substitution. Employees may utilize the time savings to clear workloads, generate more exhaustive outputs, or participate in more roles. In the long run, firms can develop procedures, alter occupational structures and trim hiring in exposed positions. The lack of sizable employment impacts in the initial years of chatbot installation argues against a swift implosion, but does not prove it to be settled in the long term.

Entry-level jobs are especially critical. Young employees do many codifiable tasks from which they may build experience and tacit knowledge. AI can be a complement to inexperienced workers, guiding their work immediately and therefore at a lower cost to firms than on-the-job training, enabling its use to a greater range of labor market entrants.[15] It can also cut back on the number of apprentices needed; experienced workers get their routine work done faster. The fiscal implications are even more far-reaching: weaker entry routes diminish lifetime income, revenue taxes and the future stock of skilled workers.

Creation of new tasks is the key to the long-term saturation of automation as a force. Adoption of artificial intelligence (AI) gives rise to work in the areas of workflow design, model interpretation and evaluation, data governance, security, compliance, customer interaction and specialized applications.[16] It may also render feasible services that were previously unprofitable, broadening appeal for human interaction and cognition. However, it will not necessarily draw forth labor in equivalent quantity, geography, remuneration and output access. A handful of top-tier specialists can be present alongside disappearing labor in routine intellectual work. The crucial issue is whether the new and expanded activities generate adequate labor demand to sustain the overall wage pool as a share of output. Thus, the available evidence tends to accept a conditional proposition. Output expansion will offset displacement where demand is elastic, competitive pressure transmits cost savings onto consumers, complementary stimulating investment exists and workers are able to move into less exposed or newly created tasks. Replacement will dominate rather than complement where demand is saturated, production is standardized, output cannot expand and adoption is mainly focused on cost reduction. There is no support for either universal complementarity or universal replacement.

3. Are Productivity Gains Passed Through as Wages, Retained as Profits, or Transferred to Technology Suppliers?

A productivity gain creates an economic surplus without indicating the ultimate beneficiary. Where an AI-enabled employee takes four hours for work that previously required eight, the saving may turn into a larger payroll, a lower customer price, a larger corporate margin, extra output, a technology-service payment, or a higher shareholding valuation. Its distribution hinges on labor bargaining, the degree of competition, the ownership structure, buyer power and the supply of complementarities. For the state, the ultimate distribution matters as much as the gross increase since each form of income hits the tax machinery in distinct ways. Workers gain where AI increases their marginal productivity and labor-market institutions convert those gains into income.

Customer-support evidence suggests that AI can transmit expertise and improve the output of inexperienced workers, perhaps expanding access to productive employment.[17] The EIB firm research finds higher wages among AI adopters, although some of the association can be explained by traits of adopting firms and their personnel. By contrast, Danish administrative data have no measurable average earnings increase in the initial two years of AI adoption, with no measurable change in recorded hours.[18] Overall, the evidence suggests wage pass-through is feasible but neither instantaneous nor assured. Bargaining power decides whether productivity results in pay. Workers receive a larger share where complementary skills are scarce, job opportunities are high, collective bargaining extends to innovation and it's still performance-related pay. Firms win a bigger slice where workers can't monitor improvement in productivity, job opportunities are limited, or AI frees up labor. The very same technology can thus both tighten performance pay gaps and widen internal income gaps of occupational groups. The worst-performing workers may get more productive, but at the same time, engineers, domain experts and managers who are able to put AI to work may take the lion's share of wage premiums.

Consumers realize benefits through lower prices, quicker delivery of services, a wider product range, or better service quality. Consumer returns can therefore lead to an increase in real living standards despite static nominal income. Consumer surplus, however, is not directly taxed.[19] It enters into revenue when lower prices release income for other taxable spending, or if improved services lead to a rise in the volume of taxable transactions. The fiscal capture from a large consumer return can then be weak. Adopting firms keep the gain if competition is sparse, or prices are sticky, or AI is embraced, which makes internal processes more effective, whose gains are not readily observed by customers. Retained gains might show up as higher operating margins, cash flow, or investment in further intangibles. Direct taxation on the domestic taxable profit may grow if the gain is implemented in an approximate proportion within the economy. However, the overall productivity advantage and once-off domestic taxable gain are not ipso facto the same. Businesses need to pay for the supply of models, software, cloud services and consulting and integration, as well as complementary capital. These costs imply that the size of the surplus left to the adopter will be conditional on the expenditures made by the adopter.

Technology suppliers form their own claims. There are many forms of purchase. AI is often bought on a subscription. It is bought on a usage-based contract or a license through cloud services, enterprise software and licensing. A local provider may enjoy having a higher revenue per employee, at the same time as it gives away most of the added value to an upstream supplier. If this supplier is foreign, the domestically paid sum reduces domestic taxable profit and generates supplier income abroad.[20] The country can still benefit in terms of wages, consumer surplus and, as long as downstream competitiveness exists, the figures used to measure national productivity can exaggerate the part of the surplus that can exist in the corporate tax structure. Supplier capture is affected by market structure. Convergence of models and complementary services in a commoditized market could hold down prices, shifting more of the surplus to adopters and consumers. While economies of scale, proprietary data, switching costs and distribution premiums tend to reinforce market power in favor of technology suppliers, early adopters might pay a premium for the limited services available in a nascent market and, as the phenomenon diffuses, advantages accruing to technology suppliers might diminish.

Shareholders are paid the residual value of expected future profits. Gains from AI may be capitalized into equity prices prior to accounting income or dividends. The taxation of this value will be very different from payroll. Wages are normally taxed on an ongoing basis by withholding and social contributions. Capital gains can be taxed on a realization basis, at a lower rate, in a different jurisdiction, or not at all in some institutional or tax-privileged arrangements.[21] A productivity improvement can therefore increase private wealth without delivering an equivalent current flow of revenues domestically. AI-complementary workers in short supply form an intermediate category. Their compensation is legally labor income, although part may reflect scarcity rents. The key fiscal inference is that governments do not tax productivity as an abstract concept. They tax the wages, profits, dividends, realized gains and consumption through which the surplus is allocated.

4. How Might AI Shift the Labour Share?

AI share is not an officially established 'national-accounts' concept; it's a useful heuristic. It refers to that part of value added[22] that flows to AI-related capital, intellectual property, technology suppliers and economic rents after the extraction of labor compensation. Labor share is defined as employee compensation (sometimes with the addition of an adjustment for the labor share of self‑employment), as a share of value added. The research issue is whether and, if so, where and how AI influences this share. Five mechanisms alter the direction. Augmentation creates more output per worker and maintains or increases labor share if the benefit occurs alongside proportional wage increases. Substitution decreases the need for labor, exerting downward demand pull on the share. Scale expansion may restore labor demand if the lower costs induce enough additional output. The creation of new tasks supports labor income, though the creation of activities where the worker maintains the comparative advantage. Concentration of rent enables either the investor or the upstream supplier to convert its creation of productivity into profit. It turns on the relative power of the mechanisms, not the technical exposure.

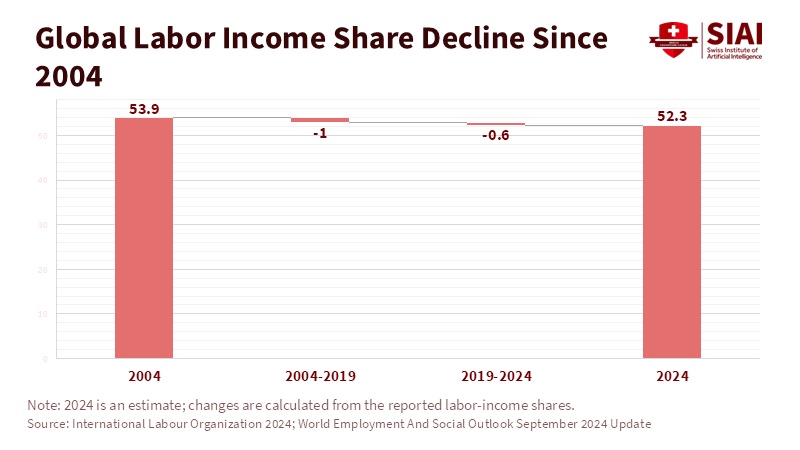

There is as yet no reliable empirical measure indicating that generative AI has brought down the economy-wide labor share by a quantifiable observed amount. Adoption is recent and measurement remains inconsistent and labor shares are subject to sectoral composition and business cycle effects, housing income, self-employment and transnational accounts. The global share of labor income had already begun heading down even before the current generative systems became widespread in their use. The ILO estimates that the global labor-income share fell from 52.9 percent in 2019 to 52.3 percent in 2022 and remained broadly unchanged through 2024,[23] but this longer-term trend cannot be traced to generative AI; it merely shows that labor entered the AI era without an irrefutable claim on productivity. Model-based analysis provides a cautious indicator of what scale we might expect: Acemoglu's upper-bound scenario assumes a small increase in the share of capital and a fall in labor's share, assuming that the impact of AI on output exceeds the growth of wages in the economy.[24] The resulting shift is comparable to small fractions of a percentage point rather than the sharp decline as postulated at times in the public discussion.

Labor-share pressures are likely to be more visible in particular sectors than in the aggregate. Administrative support jobs, hidden in well-often concentrated in protected sectors, have generative-AI exposure and may be more easily measured and improved than other work tasks, as they involve repetitive tasks, which are relatively cheap to automate.[25] For example, simple computing tasks like data entry, calendar planning, routine filing, accounting and copying may be affected proportionally. As the demand for this underlying service is likely to be fixed in each task, the source of the decline in employment in administrative jobs is likely to be primarily reduced pay bills, rather than increased output. They are one of the clearest early signs of a decline in labor share. Finance, insurance, accounting and legal services are somewhat more mixed. Text, data and pattern-recognition tasks generate far more exposure, yet regulation, fiduciary duties, model risk and client confidence preserve important human roles. Jobs may stay relatively stable while importance is added and profit-per-partnership or shareholder increases faster than costs. Labor share thus can fall without mass layoffs. Within a business, junior roles may shrink while senior staff and rare technical professionals benefit from extra income.

Public services need a different measure. If a tax office, hospital, school, or local authority handles many more cases with the same number of staff, there's a chance that measured labor share will hardly fall, because output in the non-market is often based on input prices.[26] Productivity improvement might take the form of fewer queues, better quality or efficiency, not higher 'market' profit. Standards of national labor-share figures could underestimate salient fluctuations in productivity in the public sector. The other factor is firm heterogeneity. As shown by the EIB evidence, productivity growth is heavily biased towards medium and large data, capital, software and skilled- worker intensive adopters.[27] Such productivity growth is potentially accompanied by market share shifts away from less productive small companies and a resulting reduction in aggregate labor share because the less productive small companies are more payroll-intensive than they are value-added-intensive. On the other hand, new, less costly AI tools may remove at least some competition barriers for small companies, the self-employed and independent professionals, thus avoiding income concentration.

The falling labor share does not necessarily mean real wages are falling. Wages may rise with a smaller share of a faster-growing total. Consumers may gain via lower prices. The fiscal worry is that governments tax wages/employment contributions sooner and more smoothly than retained earnings, unrealized capital gains, or border-crossing supply of income-that is, a small shift in factor shares may lead to a much larger shift in revenue composition, destination and timing. The current evidence belies any assertion of a sharp collapse in the labor share, as well as the presumption that distributional impacts are minor. Nor can any aggregate shift caused by generative AI be established, but significant reallocations at the firm and sector levels seem feasible and could be underway already. The key variables are payrolls as a share of value added; wage growth relative to labor productivity; entry-level employment in new firms; domestic operating profits; payments for imported technology services; and the generation of new labor-intensive jobs. Exposure indices simply cannot determine the extent to which the labor share will decline.

5. Are the Resulting Wages and Profits Taxable Where Affected Workers and Customers Reside?

The most direct channel is personal income tax. If AI raises wages and employment, then taxable labor income increases. If firms cut hours, cut hiring, or automate, there are larger cutbacks in the base. Since top personal income tax schedules are progressive, distributional effects matter. Substantial redistributions to a small number of highly skilled specialists might generate large revenue, but may be offset by large layoffs among middle-income employees when allowances, thresholds and behavioral responses are taken into account. Employee and employer social contributions are especially vulnerable as they are formally linked directly to pay and used to pay for pensions, health care, unemployment insurance and other benefits.[28] The bottom line for contribution bases can be eroded even if aggregate national income rises if compensation is shifted from wages to profits. Contribution ceilings may aggravate the problem by providing tax shelter above a cap for highly paid workers without generating any further revenue. A broad-based increase in middle-income wages is monetarily different from a similar total increase concentrated among a handful. Payroll taxes are subject to the same logic. They are mostly tied to the place where the worker works and collected on an ongoing basis, so that they are, in effect, more stable and less mobile.

Corporate profits and capital income are more concentrated, more volatile and sometimes more globally mobile.[29] A government may indeed hold on to total revenue during an initial AI-driven expansion while substituting a large labor base for a narrow profit base and its distinctive cyclicality. When the lost payroll adopters keep the productivity gain as a domestically taxable profit, their corporate-income-tax receipts can offset the losses in payroll. Reduced labor costs, enhanced output and improved margins all raise the corporate obligations. But this offset is not automatic; taxable profit depends on the ways a firm can manage its deductions, losses, financing, depreciation, investment incentives and where it claims income. A few dominant corporations may dominate corporate receipts, a source of increased volatility and political liability. It also needs to be separated from payments to suppliers of the technology. Even a domestic firm can have had higher productivity in the home market but paid huge sums for foreign models, cloud services, software, integration, or IP, which eat into the profit that remains at home. The adopting country can continue to gain from wages, lower prices and higher competitiveness, but gross productivity growth will overstate the corporate income tax that can be levied by the government when so much has been exported to foreign suppliers.

Dividends and capital gains also offer another revenue stream. Increasing profits can be shared directly as dividends, or capital gains can increase to the extent investors anticipate future profits. Capture through capital gains is a function of the investor's residence and ownership, realization rules, exemptions and timing. Capital gains can be unrealized for years, can be expatriated, or can be held through pension funds and other tax-privileged vehicles and the requisite future tax receivable embedded in an equity valuation cannot fund today's unemployment benefits, retraining, or pensions in exactly the same manner as a monthly payroll withholding. The consumption tax only indirectly takes some of the gain. Rising real wages, dividends, or corporate profits may enable more household expenditures. Falling prices can raise real buying power, freeing income for other taxed purchases. However, surpluses are not themselves taxed. If AI lowers a taxed service price, with a fixed quantity, value-added tax revenue may fall. Spending the savings on a different good may restore overall VAT returns. This effect is driven by observed nominal expenditure, not uplift in consumer welfare. Public expenditure can increase during adjustment. Those displaced from exposed occupations may need unemployment insurance, income security, retraining, job-search assistance and mobility programs. Aggregate employment stability does not remove this cost, since disruption may be absorbed by individual occupations, geographic areas, or ages. An important national effect can have a profound local adjustment. Ineffective retraining, which produces costs without improvement in employment, should also be taken into account.

AI can also boost the public balance sheet through tax administration and public-service efficiency. Against a background of expanding data collection, tax authorities are increasingly harnessing AI and big data-driven systems to improve risk management, limit tax evasion and avoidance, select cases and provide services to taxpayers. OECD evidence indicates that a large majority of surveyed tax administrations by 2023 were either already exploiting or in the process of deploying AI.[30] Better targeting can drive compliance, increasing revenue and cutting collection costs; automation of routine administration can release officials to concentrate on more complex cases. These improvements will depend on quality data, supervisory human oversight, cybersecurity, legal protection and sophisticated procedures for challenging automated judgments. These benefits should be viewed as a potential fiscal offset, rather than a windfall. The three hypothetical 100 productivity-gain cases do show the importance of incidence. They are stylized accounting cases, not empirical estimates or forecasts. Assume that there is also a 20 percent tax on the additional wages, 10percent on the incremental domestic profit and the consumer-benefit component produces an illustrative VAT effect of 10 percent. The VAT assumption does not reflect the direct taxability of consumer surplus; it is just a simplified increase in taxable expenditure with regard to the benefit.

In Case A, €60 appears as wages, €30 as domestic profit and €10 as consumer benefit. Wage tax yields €12, profit tax €3 and VAT €1, producing total domestic revenue of €16. This is the widest base, widest in the sense that almost all of the gain ends up as domestic labor income. In Case B, €20 goes to wages, €60 to domestic profit and €20 to consumer benefit. The effect of wage taxes is €4, profit taxes €6, VAT effect €2, thus €12 in all. Corporate revenue is higher than in Case A, but not enough to offset the weaker labor base, assuming these tax rates. In the simple example of Case C, €20 goes to wages, €20 to domestic profit, €40 to payments to foreign AI suppliers and €20 to consumer benefit. If in this case we suppose no direct domestic tax collection on the foreign income outside the model, the wage is taxed at €4, the profit is taxed at €2 and the VAT effect is €2, totaling €8 in domestic revenue. The same €100 gross productivity advantage produces only one-half the revenue of Case A in this case because a relatively much greater share appears outside of the model's assumed domestic base.

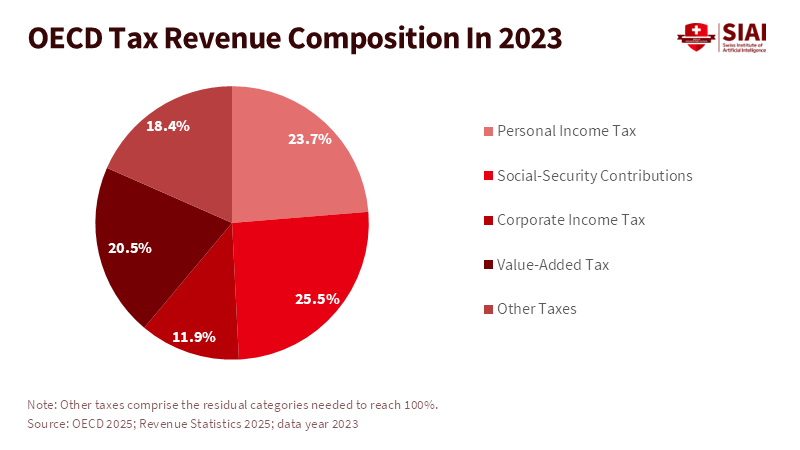

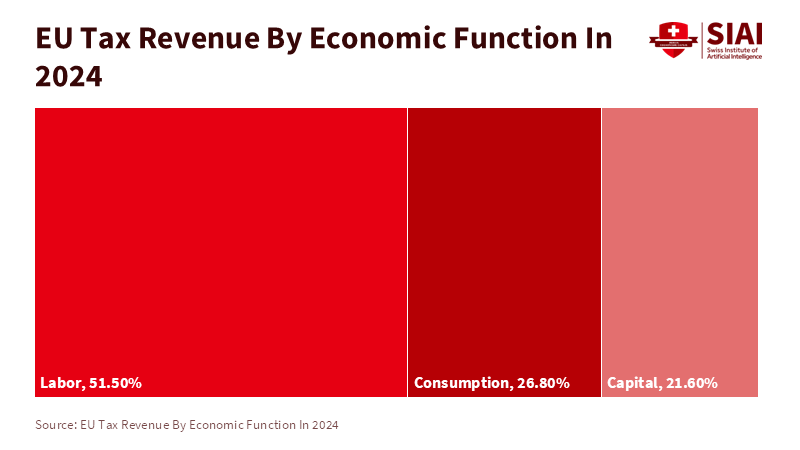

These scenarios do not prove that AI will cut government revenues by 50 percent. They do not allow for progressive rates, social contributions, deductions, investment, supplier payroll, withholding taxes, 'trade' effects, behavioral responses and deferred taxation of capital gains. They accept the full €100 as available surplus, although real adoption implies complementary spending. Their purpose is narrower: calculating fiscal projections on the basis of GDP or productivity alone can be highly misleading when the distributional and 'jurisdictional' aspects of the gain are neglected. Current tax arrangements are therefore relevant to this composition problem. Personal-income taxes and social-security contributions combined constitute a significantly larger proportion of total revenues than do corporate-income taxes throughout the OECD.[31] Within the EU, taxes on labor (including social contributions) constitute roughly half of total tax revenue.[32] A continuing transfer of revenues from payrolls toward profits or capital gains or to foreign providers may harm the bases upon which social insurance and other public services are paid, even if GDP continues to grow.

Tax treatments might also shape the adoption path. In their model of a sub-optimally high automation rate, Acemoglu, Manera and Restrepo show that the US tax system taxed labor more heavily than capital over the course of the last century, thus incentivizing automation above the socially optimal level.[33] However, it must be noted that this study deals with automation as a whole, rather than production using generative AI specifically and reaches its conclusion on the basis of a set of assumptions made in the model. Nevertheless, it sends a clear message: tax policies should not unintentionally incentivize labor substitution in an artificially attractive light relative to augmentation, organizational change, or skills acquisition.

Measurement remains a central fiscal institution. Departments of finance, statistical offices, tax authorities and social-insurance agencies require linked data on firm-level adoption, payrolls, occupations, wages, sales, profits, imported services and the taxes they pay. Circumstances where firms have furloughed, increased wages, or transferred the proceeds abroad cannot be identified from aggregate exposure indices alone.[34] Within sector monitoring must compare observed developments with what technical potential permitted while monitoring flows into entry-level jobs, contribution density, a firm's labor share and intermediate supplier expenditure. Transition policies should be based on actual displacement, not on conjectural estimates of national employment figures. Unemployment insurance and income support are required where displacement takes place and retraining should be related to credible labor demand and assessed by subsequent employment and earnings. Short-term wage insurance may be more appropriate for a few mid-career workers than long classroom courses. Policies should be amplified where verified displacement increases and changed if labor demand resurges. Thus, AI may boost corporate revenue at the expense of wages, increase tax compliance at the expense of adjustment costs and improve consumer well-being at the expense of rent-sharing. The tax problem is not merely a single change in the base but one in the composition, timing, localization and jurisdiction of revenue.

6. Which Fiscal Structures Are Most Exposed?

The highest fiscal risk occurs where a number of vulnerabilities combine. High dependence on labor taxes alone is inadequate because employment and real wages could increase if augmentation succeeds. High occupational vulnerability alone will also be inadequate, because exposed jobs can be converted into other types of occupations. The greatest danger exists if all six of the following factors reinforce one another: high dependence on labor taxes; available substitutions of cognitively based employment; weak capital-income tax payments; low domestic ownership of capital stock; payments to foreign producers of technology; and rising expenditure pressure. Employers are hit directly by social-contribution systems as they fund them through payroll. The share of social-security contributions in total tax revenue in 2023 was over 40 percent in Czechia, Slovenia and Slovakia.[35] While these economies might not be the most exposed to generative AI in employment terms, especially where manufacturing is still relevant, the impact in fiscal terms is clear. A shift in the value-added composition from payrolls to profits or imported services undermines the funding base of pensions and social-insurance systems directly.

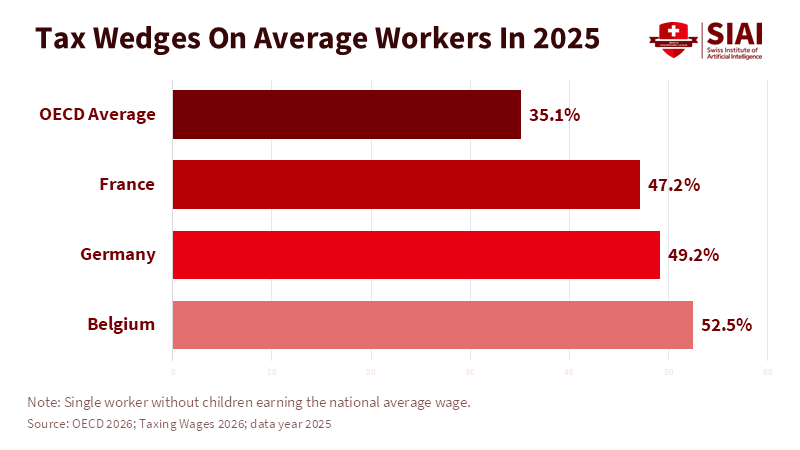

An analogous situation exists among countries exhibiting high tax wedges on formal employment. Belgium, Germany, France and Austria all register some of the highest totals of personal and social contributions borne by the typical worker of the OECD.[36] Again, a high tax wedge on employment does not necessarily point to a net employment effect of AI; it simply emphasizes that every euro taken away from the wage bill requires the outflow of much profit and capital income. If these are taxed less than current income forms, the tax effect of diversion increases. A similar sort of risk is represented by countries whose reliance on personal-income taxes, as opposed to social contributions, is especially pronounced. Denmark is just such an example, with significant levels of government revenues coming from the former while contributing less to the latter. Its highly digitized labor market entails significant technical exposure, but high levels of general consumption taxation, an efficient administrative bureaucracy and effective labor-market institutions are compensating factors. This sheds light on just why exposure should not be ranked within only a single tax category.

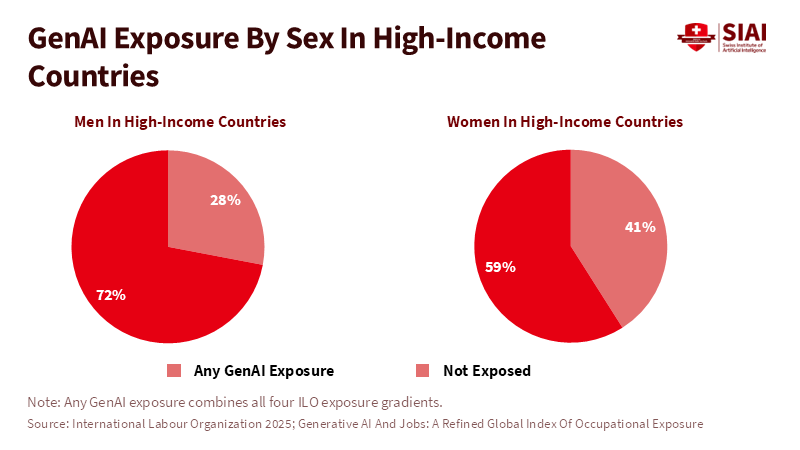

The highest amount of occupational exposure is likely to exist in service-intensive high-income economies. According to the ILO, 34 percent of employment in high-income states has at least some generative-AI exposure, relative to 11 percent in low-income states. In these economies, there is a fairly large prevalence of clerical, financial, professional, technical and administrative jobs, many of which have relatively high wages, meaning these economies could garner the most benefit from productivity but could also see the most significant movement away from broad labor compensation if rent concentration and substitution take hold.

Another distinct vulnerability arises if domestic ownership is weak. While a country can quickly utilize the AI to boost productivity and consumer benefits , payments for technology will be made to foreign owners, which will shrink the domestic operating surplus and needed capital income base and enhance "ownership income" in the homeland less than what would be reflected in the productivity figures. Firms, cloud providers, software and other intellectual properties have mostly foreign owners, though the business and capital stocks could grow less than the productivity data would indicate. The IMF scenario estimates help distinguish economies that produce and own important AI assets from those that only import these services, while acknowledging the scenario's nature.[37] Ownership should not be conflated with the physical location of the infrastructure. A state can host infrastructure and not be the owner of the most sophisticated models, software, or intangible assets and a domestic firm can own artificial intelligence assets while contracting for infrastructure services outside. In terms of fiscal incidence, the key variables are the recipient of the income, the contractual form of the transaction and the jurisdiction of the taxation of profit or capital income. An infrastructure nexus so detailed belongs to a different tax question.

In countries with only weak effective tax on capital and profits, exposure increases even with AI rents remaining within the economy. Changing from wages to retained profits, dividend income, or capital gain tax will lessen revenue where that source is either exempt, deferred or weakly enforced; and statutory corporate tax rates will be just half of the factor. Tax expenditures and old-style profits-for-years-with-no-tax arrangements, with institutional ownership and realization-based capital gains provisions, alter collection. Highly profitable economies can be susceptible in this way and multinational nodes can generate significant revenues through large, highly concentrated sets of firms, thus allowing profit taxes to offset a feeble labor force. However, reliance on such a limited and heavily internationalized pool is itself subject to fluctuations in the decisions of multinational enterprises. Ireland and Luxembourg should not be treated simply as weak-profit-tax jurisdictions. Their potential exposure to risk might stem from concentration and mobility rather than weakness.

All revenue sources are made more susceptible by aging and debt. In countries with growing pension, health care and long-term-care costs, a decline in contribution income in itself or an erratic tax portfolio will have harsher revenue consequences than the same or smaller downturn in payrolls for a more youthful, less indebted economy. The European Commission's aging projections are built-in scenarios based on what-if demographic and policy assumptions, but they clearly demonstrate the cost squeeze European countries face in future decades.[38] A small permanent weakening of payrolls in such a macroeconomic environment could be much more harmful than a temporary large disturbance to a younger population in a more lightly indebted country.

Cross-country fiscal evaluation, consequently, must involve many indicators. Countries should assess their reliance on labor taxation and social contributions, the skill composition of the formal sector, the true take-up and labor market responses, the effective taxation of profits and capital income, payments to foreign technology providers, domestic ownership of productive assets and the medium-term budgetary and debt constraints. There is no one measure of exposure. The existence of national stress tests can incorporate alternative distributions of incidence without assuming the ability to predict technological advances: in an all-wage scenario, an augmentation model may take full wage pass-through; in a high-corporate-profit model, a declining payroll and rising domestic corporate income model may be applied; in an imported-rent model, a significant share of suppliers receiving international payments can be incorporated. Each should apply the appropriate personal tax schedule, contribution system, effective corporate rates, consumption taxes and benefit expenditure schedule and be cast as conditional ranges that should be refined iteratively as administrative data improves.

Policy should match the diagnosed vulnerability. Payroll-dependent countries should monitor wage pass-through, contribution density and entry-level employment; weak capital income taxation requires broader effective capture, rather than a special AI levy; AI-service importers require better data on technology payments and a greater share of home value added. Heavily indebted and aging relies on contingency planning for adjustment costs and revenue volatility. Tax administrations can benefit from AI for ensuring compliance, while not compromising due process, transparency and human accountability. Pretax fiscal incidence is also affected by the provision of labor-market institutions. Institutions such as training, portable social insurance, efficient job matching, collective bargaining and competition can provide augmenting and scale-expanding effects. They do not just serve as reinforcing improvements after the shrinking revenue base has occurred. Instead, they influence whether higher productivity is revealed in increased wages, job creation, consumers’ gains or concentrated rents. The most durable fiscal cushion will not result from heavier taxation of a declining wage bill, but from a healthy economy where rising productivity is reflected in and taxed from widely spread, domestically generated income. Countries most exposed are those in which the gains will be incorporated into forms that the domestic fiscal system captures weakly, slowly, or not at all, while public obligations remain tied to employment, aging and social insurance.

7. Conclusion - When Does AI Expand Rather Than Erode the Tax Base?

Artificial intelligence does not mechanically erode the tax base. It shifts the tasks that produce income and can enhance productivity, wages, corporate profits, aggregate consumption and fiscal administration. Preliminary evidence suggests significant productivity gains in selected tasks and significant workplace exposure, but not a general job-shedding in the economy. The strategic risk is a divergence of productive capacity relative to domestic fiscal capture. An economy may gain productivity while shifting a broad, immediately taxed payroll base toward concentrated profits, deferred capital gains and revenue from foreign suppliers. High wage pass-through, competitive diffusion, new-task creation and growth of domestic enterprise can produce the opposite outcome as well. Governments must avoid complacency on the one hand and destructive technology-specific taxes on the other and should base intervention on measured rather than speculative displacement. Fiscal resilience will depend less on headline productivity improvement than on the extent to which the income generated by that productivity is distributed broadly and locally and ultimately able to be taxed.

This article was prepared as an independent research contribution following Professor Keith Lee’s presentation at the conference Inequalities in Longevity, held at Fondazione Giorgio Cini in Venice on 3–4 July 2026, and a subsequent substantive discussion with Federico Fubini of Corriere della Sera. The discussion helped sharpen the motivating questions concerning AI-driven productivity, the declining employment intensity of economic growth, and the resulting pressures on the public tax base.

The research, analysis, and conclusions were developed independently by the author. This publication is separate from the official conference proceedings and from the editorial coverage published by Corriere della Sera.

Unless expressly stated otherwise, this publication has not been commissioned, reviewed, or endorsed by Fondazione Giorgio Cini or Corriere della Sera. References to the conference and the subsequent discussion describe the intellectual context in which the research developed and do not imply co-authorship, institutional affiliation, formal collaboration, or partnership. The analysis, interpretations, and conclusions are those of the author and do not necessarily reflect the official positions of Fondazione Giorgio Cini, Corriere della Sera, the Swiss Institute of Artificial Intelligence (SIAI), or their respective affiliates.

References

[1] Noy, S. and Zhang, W. (2023) ‘Experimental evidence on the productivity effects of generative artificial intelligence’, Science, 381(6654), pp. 187–192.

[2, 15, 17] Brynjolfsson, E., Li, D. and Raymond, L.R. (2023) Generative AI at Work. NBER Working Paper No. 31161. Cambridge, MA: National Bureau of Economic Research.

[3] Dell’Acqua, F., McFowland III, E., Mollick, E.R., Lifshitz-Assaf, H., Kellogg, K.C., Rajendran, S., Krayer, L., Candelon, F. and Lakhani, K.R. (2023) Navigating the Jagged Technological Frontier: Field Experimental Evidence of the Effects of AI on Knowledge-Worker Productivity and Quality. Harvard Business School Working Paper No. 24-013. Boston, MA: Harvard Business School.

[4, 5, 6, 25] Gmyrek, P., Berg, J., Kamiński, K., Konopczyński, F., Ładna, A., Náfrádi, B., Rosłaniec, K. and Troszyński, M. (2025) Generative AI and Jobs: A Refined Global Index of Occupational Exposure. ILO Working Paper 140. Geneva: International Labour Organization.

[7, 24] Acemoglu, D. (2025) ‘The simple macroeconomics of AI’, Economic Policy, 40(121), pp. 13–58.

[8, 18] Humlum, A. and Vestergaard, E. (2025) Large Language Models, Small Labor Market Effects. NBER Working Paper No. 33777. Cambridge, MA: National Bureau of Economic Research.

[9, 13, 14, 34] Hampole, M., Papanikolaou, D., Schmidt, L.D.W. and Seegmiller, B. (2025) Artificial Intelligence and the Labor Market. NBER Working Paper No. 33509. Cambridge, MA: National Bureau of Economic Research.

[10] Autor, D.H. (2015) ‘Why are there still so many jobs? The history and future of workplace automation’, Journal of Economic Perspectives, 29(3), pp. 3–30.

[11, 12, 27] European Investment Bank (2026) EIB Group Investment Survey 2025/2026. Luxembourg: European Investment Bank.

[16] Acemoglu, D. and Restrepo, P. (2019) ‘Artificial intelligence, automation and work’, in Agrawal, A., Gans, J. and Goldfarb, A. (eds) The Economics of Artificial Intelligence: An Agenda. Chicago: University of Chicago Press, pp. 197–236.

[19] Brynjolfsson, E., Collis, A. and Eggers, F. (2019) ‘Using massive online choice experiments to measure changes in well-being’, Proceedings of the National Academy of Sciences, 116(15), pp. 7250–7255.

[20, 21, 28, 29, 37] International Monetary Fund (2024) Broadening the Gains from Generative AI: The Role of Fiscal Policies. Staff Discussion Note 2024/002. Washington, DC: International Monetary Fund.

[22] ILOSTAT (2024) Labour Income Share as a Percent of GDP: ILO Modelled Estimates and Methodological Description. Geneva: International Labour Organization.

[23] International Labour Organization (2024) World Employment and Social Outlook: September 2024 Update. Geneva: International Labour Organization.

[26] European Commission (2013) European System of Accounts: ESA 2010. Luxembourg: Publications Office of the European Union.

[30] Organisation for Economic Co-operation and Development (2024) Tax Administration 2024: Comparative Information on OECD and Other Advanced and Emerging Economies. Paris: OECD Publishing.

[31, 35] Organisation for Economic Co-operation and Development (2025) Revenue Statistics 2025. Paris: OECD Publishing.

[32] European Commission (2026) Data on Taxation Trends. Brussels: Directorate-General for Taxation and Customs Union.

[33] Acemoglu, D., Manera, A. and Restrepo, P. (2020) ‘Does the US tax code favor automation?’, Brookings Papers on Economic Activity, 2020(1), pp. 231–300.

[36] Organisation for Economic Co-operation and Development (2026) Taxing Wages 2026. Paris: OECD Publishing.

[38] European Commission (2024) 2024 Ageing Report: Economic and Budgetary Projections for the EU Member States, 2022–2070. European Economy Institutional Paper 279. Brussels: Directorate-General for Economic and Financial Affairs.