AI and Tax: Who Captures the Productivity Dividend?

His recent work examines the broader socioeconomic consequences of artificial intelligence, including labor markets, public finance, demographic change, institutional adaptation, and the distributional effects of technological progress.

He holds a PhD in Mathematical Finance from Boston University, and previously earned an MSc in Finance and Economics from the London School of Economics. He completed his undergraduate studies in Economics at Seoul National University under the Korea Foundation for Advanced Studies scholarship program.

Authored on

Modified

AI can create task-specific “superhuman productivity,” sharply compressing the time required for some knowledge work without implying that one person can replace ten complete jobs he fiscal risk is less an immediate collapse of government revenue than a gradual shift from broadly taxed labour income toward concentrated profits, capital income and economic rents Because those gains are more mobile across borders than payroll, governments will need stronger capital-income taxation, better measurement and international coordination rather than a blunt tax on AI itself

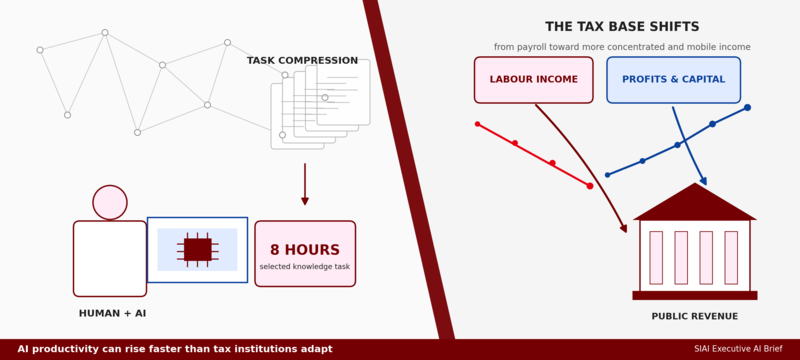

On 13 July 2026, Mr. Federico Fubini published an article in Corriere della Sera asking who will finance the state if artificial intelligence reduces the number of workers while making a smaller group dramatically more productive.[1] The article, which first appeared in his Whatever It Takes newsletter, drew on our recent interview and included my example of a student who completed in eight hours an analytical assignment that would normally have required several days. I welcomed the central question, but I also wanted the wording to remain precise. AI can compress selected tasks by several multiples; that is not the same as saying that one person replaces ten complete workers across everything they do. This brief develops that distinction and explains why it matters for taxation.

Superhuman productivity is real—but it is task-specific

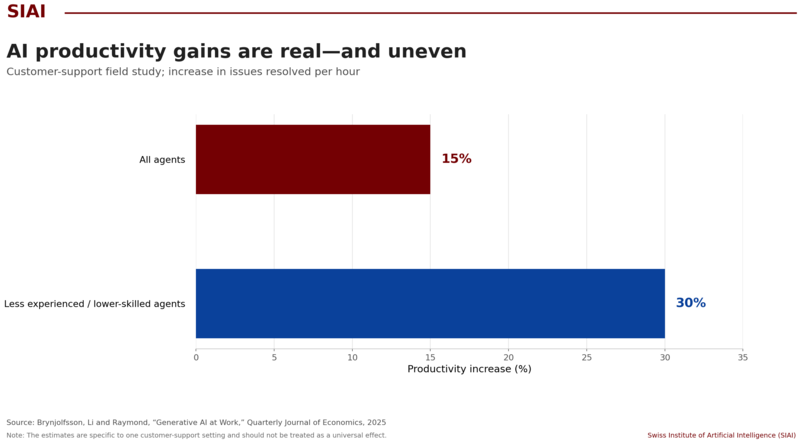

In the interview, I described what I call “superhuman productivity”: the ability of a person who understands AI tools to complete selected forms of knowledge work far faster than conventional workflows allow. The student example was striking because the assignment was substantial—20 to 30 pages, several charts and a level of analysis for which I would normally allow a week. She finished it in eight hours. The important qualification is that AI accelerated a defined bundle of tasks; it did not make the student ten times better at every part of research, judgment, communication or professional responsibility. That distinction matters because jobs are collections of tasks, not indivisible units. Evidence from workplaces points in the same direction. A large field study of 5,172 customer-support agents found that AI assistance increased issues resolved per hour by 15% on average, with gains around 30% for less experienced and lower-skilled workers, while effects for the most experienced workers were much smaller.[2] The lesson is not that a universal tenfold productivity jump is already here. It is that productivity effects can be large, uneven and highly dependent on the task, the worker and the way the organization redesigns work around the technology.

“AI can enable what I would describe as superhuman productivity in selected tasks. That does not mean one person replaces ten entire workers, but it does show how dramatically AI can compress the time required for certain forms of knowledge work.”

Correiere della Sera - Tasse, la rivoluzione dell’intelligenza artificiale: chi le pagherà se i lavoratori sono già sempre di meno? | Corriere.it

The tax base may shift before it shrinks

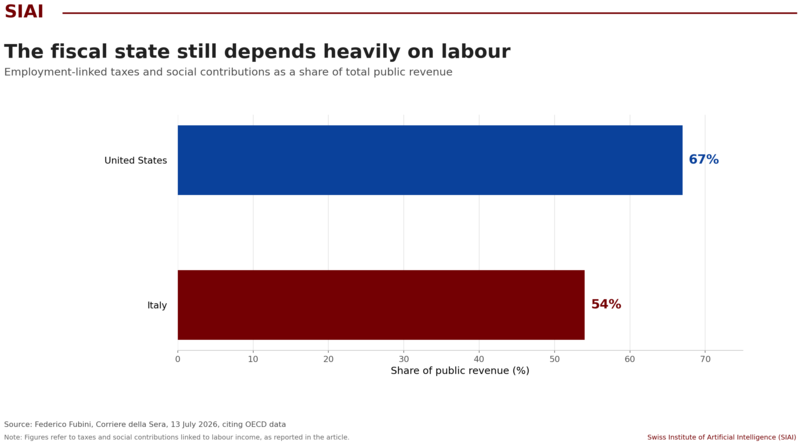

Fubini’s fiscal question is important because modern states still collect a large share of revenue from labour. His Corriere article reports that taxes and social contributions linked to employment account for about 67% of public revenue in the United States and 54% in Italy, citing OECD data.[1] I do not expect a doomsday scenario in which AI suddenly removes the tax base across the whole economy. The effects will arrive unevenly, first in activities that are digitized, standardized and rich in cognitive or administrative tasks. The ILO’s latest global assessment likewise finds that one in four workers is in an occupation with some generative-AI exposure, while most exposed jobs are more likely to be transformed than made redundant because human input remains necessary.[3] Nevertheless, even a one-percentage-point decline in revenue can be fiscally significant when governments already face rising demands for pensions, health care, defence and debt service. The more realistic risk is compositional: payrolls and broad wage income grow more slowly, while a greater share of value appears as corporate profit, capital gains, intellectual-property income or compensation for a narrow group of highly AI-complementary workers. The tax base may not disappear, but it may move into forms that are more concentrated and harder to reach.

The central issue is who captures the AI rent

When AI allows a team to produce more with fewer hours of human labour, the resulting surplus can be distributed in several ways. Workers may receive higher wages; customers may receive lower prices; firms may earn higher margins; or shareholders and senior managers may capture the gain through dividends, capital appreciation and equity-linked compensation. Which outcome occurs is not determined by the technology alone. It depends on competition, ownership, labour bargaining power, market structure and tax design. This is why I would not begin with a simple “robot tax.” A tax on the tool itself could slow useful adoption, encourage firms to disguise automation and penalize productivity-enhancing investment regardless of whether it displaces labour. The better target is the income and economic rent created by AI. An IMF staff discussion note reaches a similar conclusion: governments should prepare for disruptive scenarios, strengthen taxation of capital income and reconsider tax provisions that favor labour-displacing assets, while using social protection and education policy to broaden the gains.[4] The underlying principle is straightforward. If AI shifts income away from broadly distributed labour compensation and toward profits, capital income and market rents, the tax mix must be able to follow that shift without treating innovation itself as the taxable offence.

Purely national measures will be easy to arbitrage

The difficulty is that payroll is comparatively visible and geographically anchored, while many AI-related gains are mobile. A company can locate intellectual property, cloud contracts, financing structures or taxable profits in a different jurisdiction from the workers and customers who helped create the value. Highly paid individuals also have greater capacity than ordinary employees to relocate residence, assets or business activity. Data centres create a physical footprint, but even they can be moved toward locations with cheaper energy, favourable regulation or lower taxes, while the service remains available globally. This means that a country acting alone may impose a new charge, lose the investment and still fail to capture the underlying economic rent. International tax cooperation is therefore part of AI policy. The OECD/G20 Pillar Two framework provides a useful direction by establishing a coordinated minimum level of taxation for large multinational groups when the effective rate in a jurisdiction falls below the agreed floor.[5] It is not a complete solution: it does not settle how to allocate all AI-created value, nor does it fully address personal capital-gains mobility. But it demonstrates the institutional logic required. The more digital, intangible and concentrated the tax base becomes, the less effective purely national responses will be.

An executive agenda: measure, share and tax the gains

For executives, the first responsibility is measurement. A credible AI productivity programme should track not only output and cost savings, but also headcount, wage distribution, contractor substitution, entry-level hiring, training access and the location in which additional profit is booked. Boards should ask whether AI gains are being used to augment the workforce, remove career ladders or concentrate rewards in a small group. Governments need an equally practical dashboard: payroll-tax receipts by sector, labour’s share of value added, corporate profit concentration, capital-gains realizations and the migration of taxable income across borders. Social-insurance financing may gradually need a broader base so that benefits do not depend so heavily on conventional payroll when production relies increasingly on software, capital and small teams of AI-enabled workers. At the same time, training remains essential but cannot be the only answer; workers also need time, mobility support, portable benefits and credible pathways into redesigned roles. My conclusion from the interview is therefore neither alarmist nor complacent. We should not tax AI merely because it is AI. We should tax the income and rents it creates where they genuinely accrue, preserve incentives for productive adoption, and use part of the dividend to finance the transition. The decisive question is whether fiscal institutions can move as quickly as the technology.

Selected sources

3. International Labour Organization, Generative AI and Jobs: A 2025 Update, 20 May 2025.

5. OECD, Global Anti-Base Erosion Model Rules (Pillar Two) and related implementation guidance.

His recent work examines the broader socioeconomic consequences of artificial intelligence, including labor markets, public finance, demographic change, institutional adaptation, and the distributional effects of technological progress.

He holds a PhD in Mathematical Finance from Boston University, and previously earned an MSc in Finance and Economics from the London School of Economics. He completed his undergraduate studies in Economics at Seoul National University under the Korea Foundation for Advanced Studies scholarship program.